How Accrual Accounting Works and Why Your P&L Depends on It

June 2, 2026

Most growing companies frequently hit the same wall: the books show a profitable month, but the bank account tells a different story. I've spent the last decade mentoring finance teams, and the most common scene I walk into is the same one. A founder or COO is staring at a P&L that says the company had a profitable month, then refreshes the bank balance and sees almost the opposite.

Cash accounting creates that gap because it records money only when it moves, not when it's earned or owed. This means payroll cycles, vendor invoices, and slow-paying clients all distort what a period looks like.

In this guide, we dive into accrual accounting, explore the difference between cash and accrual accounting, and the five accrual types you'll need to know. Then we also look at how to approach the tooling decisions that determine whether your close cycle runs predictably or eats your team's weekends.

In brief:

- Accrual accounting records revenue when earned and expenses when incurred, regardless of when cash moves, which makes a P&L more useful for actual decisions than a lagging cash report.

- The matching principle pairs each expense with the revenue it helped generate, so a period's income statement reflects what the business did rather than when payments cleared.

- There are five accrual types worth knowing: accrued revenue, accrued expenses, accounts payable, prepaid expenses, and deferred revenue, and each addresses a different timing gap between economic activity and cash flow.

- The signals you've outgrown cash accounting are practical, not academic. Net-60 terms, upfront contracts, payroll cycles that cross month-end, and any conversation with an investor or lender all point in the same direction.

- Switching from cash to accrual requires filing IRS Form 3115 and making a Section 481(a) adjustment, and that's a CPA conversation rather than a solo project.

What is accrual accounting?

Accrual accounting is the method of recording revenue when it's earned and expenses when they're incurred, regardless of when cash actually moves in or out of a bank account.

Here's the cleanest way I've found to explain accrual accounting: It records revenue when you earn it and expenses when you incur them, regardless of when cash moves. The IRS frames the same idea in Publication 538, which states that income is reported in the year it's earned, and expenses are deducted in the year they're incurred.

What is the difference between cash and accrual accounting?

I can say that the biggest difference between the two is timing, which is where most operational pain shows up. Cash accounting records transactions when cash moves, while accrual accounting records them when the economic event occurs. This can produce two financial pictures of the same period that look almost unrelated.

Here are the differences at a glance:

| Factor | Cash basis | Accrual basis |

|---|---|---|

| Revenue recorded when | Cash is received | Revenue is earned |

| Expenses recorded when | Cash is paid out | The expense is incurred |

| Accounts receivable tracked? | No | Yes |

| Accounts payable tracked? | No | Yes |

| GAAP compliant? | No | Yes |

| Cash flow visibility | Shows cash directly | Requires separate cash flow tracking |

Once you're running accounts payable and receivable across dozens of vendors and customers, cash-basis accounting starts to hide your obligations from you actively.

For instance, December financials might show almost no revenue despite a major project wrapping up that month because the client hasn't paid yet, and that's usually when the operators I work with realize they've outgrown the cash basis.

Advantages of accrual accounting

If your company has customers paying on 30-, 60-, or 90-day terms (and on net-60, I stay on the hill that they're never worth it), annual software subscriptions paid upfront, and payroll cycles that span month-end, accrual accounting is built for exactly that kind of complexity.

Four benefits stand out for the companies I've helped get there:

- Financial accuracy: Your income statement matches revenue to the period it was earned, so monthly performance data reflects reality rather than payment timing.

- Working capital visibility: Accrual-based books track both what your company owes and what others owe you, giving you a real-time view of receivable aging and upcoming vendor obligations.

- Investor and lender readiness: Banks and investors expect accrual-basis financials before they'll move forward with a funding decision, making this a prerequisite for outside capital rather than a nice-to-have.

- Better forecasting: Cash accounting only reflects what has already happened to the bank balance. In contrast, accrual accounting includes future obligations and receivables, which are the inputs needed for any forecast worth trusting.

Those advantages come from a small set of recurring accounting moves worth understanding before your team sets up the chart of accounts.

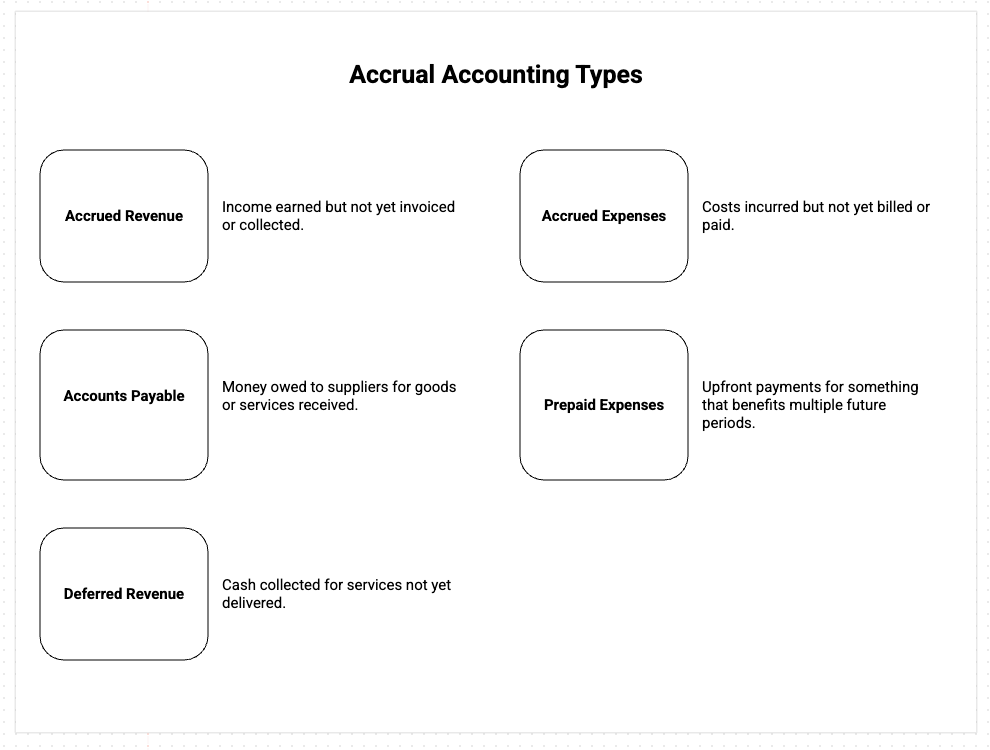

5 types of accrual accounting and how they work

Every accrual transaction follows one of two patterns. Either the economic event happens before cash moves, or cash moves before the economic event. The five types below cover every variation your team is likely to run into.

1. Accrued revenue

Accrued revenue is income you've earned by delivering a product or service but haven't yet invoiced or collected. Take the textbook example. A consulting team finishes $5,000 of work on October 30, and the client pays on November 25. The $5,000 belongs in October revenue because that's when it was earned, and in November, the entry moves from accounts receivable to cash.

What this does, practically, is keep October from understating earnings and November from overstating them. Any team billing on net-30 or net-60 terms will make these entries every month. And when a team's P&L doesn't reflect work completed during the period, missing accrual entries are usually the first place I look.

2. Accrued expenses

Accrued expenses are costs you've incurred but haven't been billed for or paid yet. Payroll is the example I've seen miscoded most often. For instance, employees earn $5,000 in the last week of December, but payroll runs in January, so the $5,000 needs to be recorded as an expense in December, with a matching entry in "accrued liabilities." When January payroll runs, the liability clears and cash decreases.

Utility bills work the same way. If your company uses $2,000 of electricity each month but pays the bill quarterly, you accrue $2,000 at each month-end, so monthly expenses reflect actual consumption.

Skipping this entry is one of the cleanest ways to make December look artificially profitable while January absorbs the full quarter's hit.

3. Accounts payable

Accounts payable is the money your company owes suppliers for goods or services you've received but have not yet paid for. Suppose $500 of inventory shows up in March with an invoice due in April, you record $500 of inventory as an asset in March and create an AP liability for the same amount. April's payment clears the liability and reduces cash.

This differs from accrued expenses because the invoice is already in hand. For operations teams managing dozens of vendor relationships, I can say that AP tracking is the only way to clearly see the next 30 to 60 days of cash obligations; without it, working capital planning becomes guesswork.

4. Prepaid expenses

Prepaid expenses are upfront payments for something that benefits multiple future periods. The classic case is annual insurance. You pay $1,200 on January 1 for a full-year policy, but the full amount cannot be applied to January's expenses.

Instead, you create a prepaid asset on the balance sheet and expense $100 each month as coverage is consumed, with the prepaid balance reaching zero by December.

The same logic applies to annual software subscriptions, prepaid rent, and any upfront payment that covers a future period. I've watched founders front-load these into the payment month, which makes that month look catastrophic and every other month look cheaper than it is.

Annual tools and insurance policies need to be carried as prepaid assets and amortized monthly, every time.

5. Deferred revenue

Deferred revenue, sometimes called unearned revenue, is cash you've collected from a customer for services not yet delivered. For example, a SaaS company selling a 12-month subscription for $12,000 upfront records the full amount as a liability on day one because the company still owes the customer 12 months of service. Each month, $1,000 moves from liabilities to earned revenue.

Recording the full $12,000 as revenue on day one is the fastest way to misrepresent a SaaS company's financial position to investors, and I've seen this on enough fundraise prep calls to flag it before anything else.

A deferred revenue schedule is non-negotiable once a company accepts advance payments, especially in the months leading up to the presentation of a cash flow statement to an investor.

Key challenges in accrual accounting and how the right accounting software solves them

Moving to accrual accounting introduces complexity that the cash basis doesn't have, and the same operational problems show up in most close cycles. In my experience, the right accounting software handles most of the manual work.

The platforms worth picking are the ones where the accrual workflow is the primary path, not an adjusting-entries pass on top of a cash ledger, and the four failure modes below all trace back to that architectural distinction.

Manual journal entries slowing down every close cycle

When someone forgets to accrue the December bonus or the quarterly utility bill, nothing in a manual workflow flags it, and the books close with one fewer expense than the period carried. By the second or third skipped entry, December's P&L starts to look noticeably better than the truth, and the comparable-period analysis the team runs next quarter is built on a number that never existed.

What good accounting software does on this front is provide templated recurring entries that post at period-end and automatically reverse upon receipt of the actual invoice. The tradeoff worth knowing is that recurring entry templates are only as durable as the chart of accounts they sit on.

Deferred revenue and prepaid schedules falling through the cracks

Every team that takes upfront payments or pays annual premiums ends up doing one of two things. Either the platform calculates the amortization schedule and posts the entries automatically, or someone on the team builds a spreadsheet that tries to do the same thing in tandem with the general ledger.

The spreadsheet version works for about two months, then drifts out of sync with the books, and by the time anyone notices the drift, it's already affected three or four revenue or expense recognition periods.

What you need is a platform with built-in deferred revenue scheduling, prepaid amortization, and an audit trail that shows how each balance was calculated. This way, investors and auditors get an answer from the system rather than from someone's memory.

Expense data living in too many places

By the time a finance team is trying to accrue the period, the upstream data has either already been captured or not, and capture decisions made weeks earlier determine whether the close runs cleanly or turns into a scavenger hunt for receipts.

I've watched teams spend the first three days of every close cycle finding the data, which is time the close didn't need to cost; for instance, in the workflow that's supposed to put a $400 client lunch into a category and an approver's queue at the time of purchase, rather than weeks later.

What I tell teams to look for here is expense management software that automates categorization, receipt matching, and approval workflows, and feeds clean data directly into the general ledger.

The honest tradeoff is that adding an expense management tool means adding an integration to the general ledger, and integrations break quietly. The teams running this stack well treat the integration as a first-class part of the close checklist rather than something to set up once and forget.

The P&L never matches the cash position

More first-time accrual converts get tripped up here than anywhere else. A profitable income statement can coexist with a shrinking bank balance because accrual accounting records revenue before cash arrives and expenses before cash leaves.

This means both reports are correct, but measuring different things, and whoever's reading them has to know which question each one answers. The mistake I see most often is treating the P&L as a cash forecast, which it isn't and never was.

Also, the cash flow statement and the AR aging report answer the "do we have the money for this" question, while the P&L can sit alongside both of them, telling a much darker liquidity story.

To solve this, the platform a finance team picks needs to toggle cleanly between accrual-view and cash-view reports so the operator sees the operational and liquidity pictures side by side without rebuilding either in a spreadsheet.

Set up the accrual foundation before your first close

Accrual accounting gives you a financial picture that reflects what happened in a period, not only what hit the bank account. The setup takes real work: the right chart of accounts, recurring entry rules, and month-end processes for each accrual type.

Here are the four things I walk every new finance team through:

- Chart of accounts: Set up separate accounts for accrued liabilities, prepaid assets, and deferred revenue from day one, not after the close cycles start breaking.

- Recurring entries: Automate payroll accruals, prepaid amortization, and deferred revenue release with templated journal entries that post and reverse on their own.

- Reconciliation cadence: Reconcile each accrual account monthly so bookkeeping errors don't accumulate across periods and turn the year-end close into a forensic project.

- CPA involvement: If you're switching from cash basis, file IRS Form 3115 and plan the Section 481(a) adjustment with a CPA, since the adjustment can create a taxable income spike that's painful to absorb if it isn't planned for.

A lot of the manual work in an accrual close cycle is chasing receipts and confirming what each vendor charge was for, so the accruals can be made cleanly.

Modern spend management platforms like Ramp handle that capture layer at the point of purchase rather than at the end of the month. Get those four right and the close cycle becomes predictable, the financials become defensible, and the P&L starts answering the questions your team asks of it.

Frequently asked questions about accrual accounting

Can you switch from cash to accrual accounting?

Yes, but you'll need to file IRS Form 3115 during the change year. The transition requires a Section 481(a) adjustment to reconcile income and expenses between the two methods, and I'd strongly recommend working with a CPA before making the change, as the adjustment can create an unexpected spike in taxable income if it isn't planned carefully.

What is the biggest risk of accrual accounting?

The biggest risk I've seen is reading the income statement as a proxy for available cash. Accrual accounting records revenue before cash arrives and expenses before cash leaves so that a profitable P&L can coexist with a shrinking bank balance. A separate cash flow statement bridges that gap by showing where the cash went, and any finance team running on accrual needs both reports on the same dashboard.

How is accrual accounting different from GAAP?

Accrual accounting is one foundational requirement within GAAP, not a synonym for it. GAAP also covers revenue recognition rules, financial disclosures, and reporting formats. Adopting accruals is the right starting point toward GAAP compliance, but it doesn't get you there on its own.

When should a growing company switch to accrual accounting?

Switch before the pressure arrives, ideally early enough to build one to two years of accrual-basis history before you need it. Offering credit terms, managing inventory, approaching a fundraiser, or applying for a bank credit line are all signals the books need to reflect economic reality rather than cash movement, and waiting until the diligence call to fix the books is the most expensive way I've seen this play out.