Best 0% APR Business Credit Cards for Growing Companies in 2026

April 17, 2026

For companies running tight on cash between invoices, or financing a major equipment purchase before revenue catches up, a 0% introductory APR business credit card can eliminate months of interest charges, but only if you understand the structure before applying.

At the current average credit card rate of 22.8% APR, a $50,000 balance carried for a full year costs more than $10,000 in interest. The right 0% APR card doesn't just give your business a window to pay down a balance interest-free. It should also match how your company earns rewards, whether you need balance transfer coverage, and how long your team realistically has to clear the balance.

This guide covers the best 0% APR business credit cards and what each one delivers beyond the introductory rate.

In brief:

- A 0% APR business credit card allows companies to finance purchases or transfer existing balances interest-free for a defined period, typically 12 to 18 billing cycles, before the standard variable APR applies.

- Ramp is the top pick for companies that don't need to carry a balance. It's a corporate charge card built for spend controls and automated expense tracking, not a revolving credit product.

- Most 0% APR business cards cover purchases only. Among these cards, only U.S. Bank Triple Cash Rewards and U.S. Bank Business Shield extend the 0% rate to balance transfers.

- The average credit card APR for accounts carrying balances was 22.8% as of 2025. A $50,000 balance at that rate costs more than $10,000 in interest annually.

- Most business credit cards require a personal guarantee. High utilization can affect personal credit scores even during the 0% promotional window.

7 best 0% APR business credit cards at a glance

Most issuers offer around 12 months of introductory 0% APR, so the real differences come down to rewards structure, welcome bonuses, balance transfer coverage, and post-promo APR. Companies that don't need to carry a balance may find a corporate charge card with built-in spend controls is a better fit than a revolving credit product.

Here is an overview of the best options:

| Card | Intro APR | Annual fee | Rewards | Welcome bonus | Balance transfers |

|---|---|---|---|---|---|

| Ramp | N/A (charge card) | $0 | Flat cash back* | None listed | N/A |

| Chase Ink Business Unlimited | 0% for 12 months | $0 | 1.5% flat | $750 after $6K/3 mo | Not covered |

| Chase Ink Business Cash | 0% for 12 months | $0 | 5% categories / 1% other | $750 after $6K/3 mo | Not covered |

| Wells Fargo Signify Business Cash | 0% for 12 months | $0 | 2% unlimited | $500 after $5K/3 mo | Not covered |

| Amex Blue Business Cash | 0% for 12 months | $0 | 2% up to $50K/yr | $250 after $3K/3 mo | Not confirmed |

| U.S. Bank Triple Cash Rewards Visa | 0% for 12 billing cycles | $0 | 3% categories / 1% other | $750 after $6K/180 days | Covered |

| U.S. Bank Business Shield Visa | 0% up to 18 billing cycles | $0 | None confirmed | None | Covered |

Each card serves a different profile. Let’s break down the specifics, including post-promo APR ranges and where each card falls short.

1. Ramp charge card

Ramp is a corporate charge card. The full balance clears every billing cycle, so there's no interest rate to manage and no option to carry a balance.

It's designed for companies that want real-time expense management controls, automated receipt matching, and native accounting integrations that reduce manual close work.

Ramp charge card pros:

- No annual fee or interest: The card requires full monthly payoff, so finance teams incur zero financing costs and face no risk of interest accruing on any unpaid balance.

- Flat cash back: Every purchase earns cash back at a flat rate without category tracking or tiered spending structures to manage.

- Built-in spend controls: Finance managers can set per-card limits and enforce expense policy automatically across every employee card in real time.

Ramp charge card cons:

- No balance carrying: Ramp cannot finance a large purchase over several months, so it doesn't serve companies that need an interest-free repayment window.

- Entity requirements: The card is generally best suited to established business entities rather than sole proprietors or newer companies with limited operating history.

Best for: If your company doesn't need to finance purchases over time and wants automated expense management with real-time spend visibility across all employee cards, Ramp is built for that.

Pricing: Ramp charges no annual fee and no interest, since the card requires a full monthly payment each billing cycle. Unlike every other card on this list, approval is based on business financials rather than personal credit history.

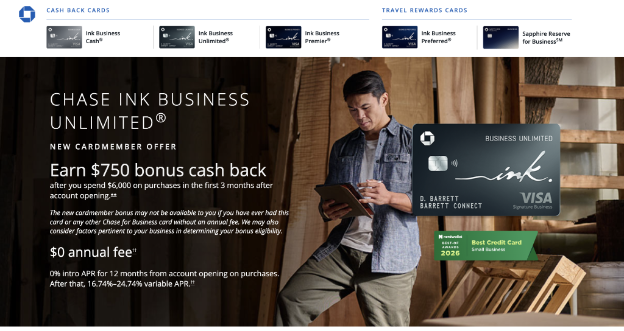

2. Chase Ink Business Unlimited

The Chase Ink Business Unlimited pairs a 12-month 0% intro APR on purchases with a sizable sign-up bonus on a no-annual-fee card.

It's the simplest business rewards card in the Chase Ink lineup, built around a single flat cash back rate with no categories to track.

Chase Ink Business Unlimited pros:

- $750 sign-up bonus: After $6,000 in purchases within the first 3 months, the card pays a $750 cash bonus, a meaningful offset against early spending costs.

- Flat 1.5% cash back: Every purchase earns at the same rate, with no categories to monitor or caps that limit rewards on higher-volume spending.

- 12-month 0% APR: The introductory period starts at account opening, giving teams a full year to pay down a defined expense without interest charges.

Chase Ink Business Unlimited cons:

- No balance transfer coverage: The 0% rate applies to purchases only, and balance transfers carry a 5% fee, making this a poor choice for companies looking to consolidate existing debt.

- 3% foreign transaction fee: Companies that make frequent payments to international vendors incur a 3% surcharge on every transaction processed outside the U.S.

- 12-month ceiling: The intro window is shorter than some alternatives on this list and doesn't suit large purchases that can't be cleared within a year.

Best for: Growing companies that want a simple flat-rate card with a large welcome bonus and don't need to consolidate existing debt.

Pricing: $0 annual fee. 0% intro APR for 12 months on purchases, then 16.74% to 24.74% variable. Approval typically requires good to excellent personal credit.

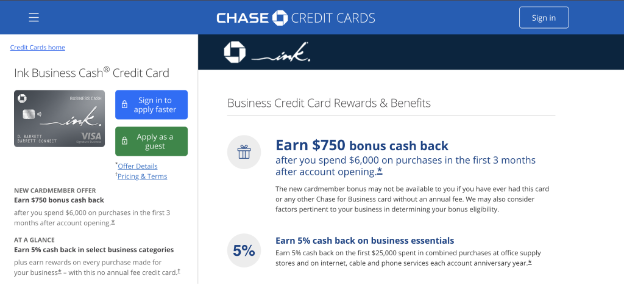

3. Chase Ink Business Cash

The Ink Business Cash shares the same 12-month 0% APR window and $750 sign-up bonus as the Ink Unlimited, but trades the flat rate for a tiered structure that rewards concentrated spending in core business categories.

It's worth considering for companies whose largest spend is on office supplies, internet services, or telecom.

Chase Ink Business Unlimited pros:

- 5% in key categories: Office supplies, internet, cable, and phone purchases earn 5% cash back up to $25,000 per year, which adds up quickly for companies with consistent spend in those areas.

- $750 sign-up bonus: After $6,000 in purchases within the first 3 months, the card pays the same $750 welcome offer as the Ink Unlimited, putting significant cash back into play early.

- $0 annual fee: No recurring card cost applies regardless of how heavily the rewards structure is used.

Chase Ink Business Unlimited cons:

- Category caps: The 5% rate applies only to the first $25,000 per year in combined bonus-category spending, so that high-volume companies may exhaust the ceiling well before year-end.

- No balance transfer coverage: Like the Ink Unlimited, the 0% rate applies only to new purchases; consolidating existing card debt is not an option with this card.

- 3% foreign transaction fee: International vendor payments face the same surcharge as on the Ink Unlimited, making this card a poor fit for globally distributed teams.

Best for: Teams that concentrate spending in office supplies, internet services, or phone plans where the 5% tier consistently outperforms flat-rate alternatives.

Pricing: $0 annual fee. 0% intro APR for 12 months on purchases, then 16.74% to 24.74% variable. Approval typically requires good to excellent personal credit.

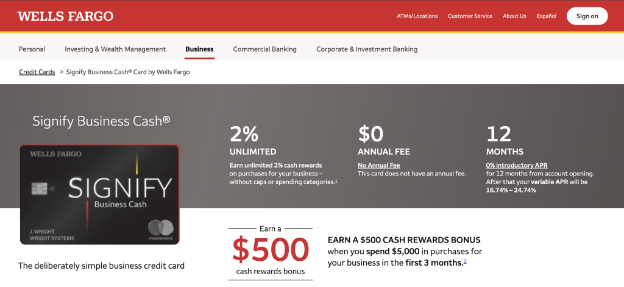

4. Wells Fargo Signify Business Cash

The Wells Fargo Signify Business Cash pairs unlimited 2% cash back on all purchases with a 0% intro APR period, no annual fee, and no spending caps or category restrictions. You can set employee spending limits, monitor cards, and more, online or in the mobile app.

Wells Fargo Signify Business Cash pros:

- Unlimited 2% cash back: Companies earn 2% on every purchase, with no enrollment requirements, category tracking, or cap that limits rewards as spending scales.

- 12-month 0% APR: The full introductory period covers purchases from account opening, giving the finance team a year to pay down a defined expense without interest accruing.

- $500 sign-up bonus: After $5,000 in purchases within the first 3 months, the welcome bonus provides immediate value for companies onboarding the card.

Wells Fargo Signify Business Cash cons:

- 3% foreign transaction fee: The card adds a 3% surcharge to any purchase made outside the U.S., which adds up quickly for companies with frequent international vendor payments. Teams with heavy cross-border spending should look at a no foreign transaction fee card instead.

- Lower sign-up bonus: At $500 versus $750 on the Chase Ink cards, the welcome offer is less competitive for companies prioritizing maximum early cash back.

Best for: If your priority is the highest flat cash back rate with no caps, no categories, and no spending tiers to manage, the Signify is the strongest option on this list.

Pricing: $0 annual fee. 0% intro APR for 12 months on purchases, then 16.74% to 24.74% variable. The $500 bonus requires $5,000 in spending within 3 months.

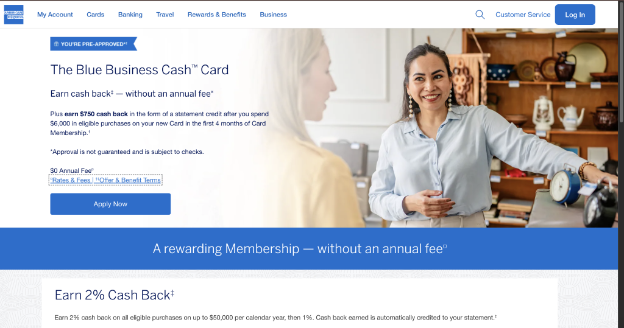

5. Amex Blue Business Cash

The American Express Blue Business Cash Card earns 2% cash back on all eligible purchases up to $50,000 per calendar year, with rewards automatically credited to the statement each month.

No portal login or redemption steps are required.

Amex Blue Business Cash pros:

- Auto-credited cash back: The 2% cash back is applied directly to the statement without any action from the finance team, simplifying reconciliation.

- $250 welcome bonus: After $3,000 in eligible purchases within the first 3 months, the standard public offer delivers immediate value for companies switching from a lower-reward card.

- $50,000 annual cap at 2%: The ceiling is generous enough that most mid-size companies spend the full year at the top rate without concern about hitting it.

Amex Blue Business Cash cons:

- $50,000 cap: Purchases beyond $50,000 in annual eligible spending drop to 1% cash back, so the card becomes less competitive for high-volume companies once they cross that threshold.

- 2.7% foreign transaction fee: Any purchase processed outside the U.S. adds a 2.7% surcharge, which materially reduces the effective cash back rate for companies with international vendors.

- Balance transfer coverage not confirmed: Amex has not confirmed 0% APR coverage for balance transfers on this card, so it is not the right choice for companies that need to consolidate existing debt.

Best for: Companies whose finance teams want cash back deposited automatically without managing a rewards portal or taking any redemption steps. The Amex Blue Business Cash removes that admin step entirely.

Pricing: $0 annual fee. 0% intro APR for 12 months on purchases, then 16.74% to 26.74% variable (will not exceed 29.99%). Approval typically requires good to excellent credit.

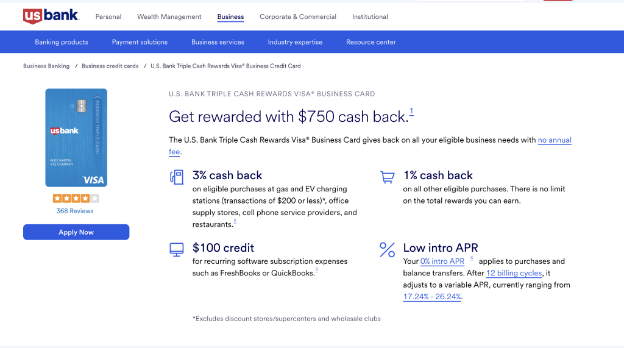

6. U.S. Bank Triple Cash Rewards Visa

The U.S. Bank Triple Cash covers both purchases and balance transfers under a 0% intro APR for 12 billing cycles. The rewards tiers target common business spending: 3% at gas stations, EV charging stations, office supply stores, cell phone providers, and restaurants, plus 1% on all other eligible purchases.

U.S. Bank Triple Cash Rewards Visa pros:

- Balance transfers covered: Both purchases and balance transfers qualify under the 0% promotional offer. This makes it one of the few cards on this list that lets companies consolidate existing debt while continuing to earn rewards.

- 3% on common categories: Gas, office supplies, cell phone, and dining earn at the bonus rate with no spending cap, so high-volume companies in those categories benefit throughout the year.

- $750 sign-up bonus: After $6,000 in purchases within the first 180 days, the welcome offer matches the best bonus available among cards in this comparison.

U.S. Bank Triple Cash Rewards Visa cons:

- 3% foreign transaction fee: International purchases face a 3% surcharge, making this card a poor fit for companies with significant cross-border vendor spending.

- Higher post-promo APR floor: The variable rate starts at 17.24%, slightly above the 16.74% floor on some peer cards. That gap matters if any balance remains after the promo window closes.

- Travel rewards limited: The 5% travel rate applies only when booking through U.S. Bank's travel rewards center, which limits its value for teams that book travel directly.

Best for: Companies that need to consolidate existing card balances while still earning rewards on ongoing expenses. It's also a strong fit if your team needs more than 12 months to pay down a large purchase and wants built-in balance transfer flexibility.

Pricing: $0 annual fee. 0% intro APR for 12 billing cycles on purchases and balance transfers, then 17.24% to 26.24% variable. Approval typically requires good to excellent personal credit.

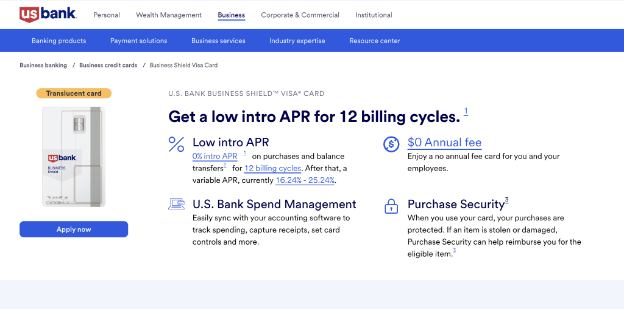

7. U.S. Bank Business Shield Visa

The U.S. Bank Business Shield Visa offers the longest introductory 0% APR window in this comparison at up to 18 billing cycles, though reaching that full term requires applying in person at a U.S. Bank branch. Online applicants receive 12 billing cycles instead.

U.S. Bank Business Shield Visa pros:

- Up to 18 billing cycles at 0%: Companies get one of the longest interest-free windows in this comparison, with enough runway to pay down a large purchase over a year and a half when applying in branch.

- Balance transfers included: Both purchases and balance transfers qualify under the promotional rate, giving companies the option to consolidate existing debt at the same time.

- $0 annual fee: No recurring cost applies even with the extended intro window, so the account costs nothing to maintain once the balance is cleared.

U.S. Bank Business Shield Visa cons:

- A branch application is required for the full 18 cycles: Online applicants receive only 12 billing cycles at 0%, so the card's main advantage requires a trip to a physical U.S. Bank branch.

- No sign-up bonus: Unlike most competitors on this list, the Business Shield offers no welcome bonus, so early spending earns nothing back.

- No confirmed rewards rate: The card prioritizes the intro window over rewards earning, with no published cash back rate for ongoing purchases.

Best for: This card is the right fit if your company is financing a large, defined purchase, a 12-month paydown window feels too tight, and you can apply in person at a U.S. Bank branch.

Pricing: $0 annual fee. 0% intro APR for up to 18 billing cycles on purchases and balance transfers (12 cycles for online applications), then 16.24% to 25.24% variable. Approval typically requires good to excellent personal credit.

How to choose the right 0% APR business credit card

Start with the question your business is actually trying to answer:

- Finance a specific purchase

- Consolidate existing debt

- Earn the best rewards during a 0% window?

If you need balance transfer coverage, your options immediately narrow to U.S. Bank Triple Cash Rewards and U.S. Bank Business Shield. If the goal is the longest interest-free runway on a large new purchase, U.S. Bank Business Shield offers the most room, provided you apply in a branch.

If your company doesn't need to carry a balance and wants to spend controls across the team, a corporate charge card like Ramp may serve you better than any revolving credit product. If you're still building business credit with limited history, verify upfront whether the card reports to business bureaus.

Before submitting any application, keep your personal credit utilization low and have a monthly payoff plan ready, since most 0% APR business cards require a personal guarantee, and high utilization can affect your score even during the 0% period.

Frequently asked questions about 0% APR business credit cards

What happens when the 0% APR period ends on a business credit card?

The card's standard variable APR begins applying to any remaining balance once the promotional period ends. Current ongoing rates on cards in this comparison run from the low teens into the mid-20% range. To avoid paying interest, build your payoff schedule to clear the balance at least one billing cycle before expiry. Paying only minimums throughout the promo window leaves the full balance exposed on the final day.

Do business credit cards have the same consumer protections as personal cards?

Business credit cards are not covered by the Credit CARD Act of 2009 in the same way consumer cards are. Issuers may have more latitude to change rates on existing balances with less notice and to revoke promotional rates more easily. Read the full card agreement before you apply and review any change-in-terms notices throughout the account's life.

Can I use a 0% APR business credit card to pay off other business debt?

Yes, but only if the card covers balance transfers under the 0% rate, and many major issuers' business cards don't. Among the cards in this guide, U.S. Bank Triple Cash Rewards covers balance transfers under the promotional offer, though a transfer fee may apply upfront.

Does carrying a balance on a 0% APR business card affect my personal credit score?

Most business credit cards require a personal guarantee, and some major issuers report at least negative activity to personal credit bureaus. High utilization can lower your score even at 0% interest. Making regular payments throughout the promo period keeps your reported balance manageable and protects your personal credit standing.