6 Brex Alternatives Finance Managers Are Switching To

June 5, 2026

Brex stopped serving most small businesses in June 2022, walking away from companies that couldn't show investor backing from a VC, angel, or accelerator. Capital One completed its acquisition of Brex in April 2026, a $5.15 billion deal that folds the platform into a much larger bank.

If you're an existing Brex customer, the change in ownership and roadmap is another reason to evaluate your options.

For companies in the 50 to 500 employee range, the replacement shortlist looks very different depending on whether you need banking and cards under one roof, deep AP automation, or a free corporate card with solid accounting sync.

In this guide, we explore the top 6 Brex alternatives in detail, compare pricing, qualification rules, accounting integrations, and who each platform is best suited for.

In brief:

- Capital One completed its acquisition of Brex in April 2026, prompting existing customers to evaluate alternatives before the platform changes take effect.

- Ramp's free tier covers unlimited cards, receipt matching, and QuickBooks or Xero sync, but it gates NetSuite and Sage Intacct behind its $15-per-user Plus plan.

- BILL Spend & Expense includes free ERP sync, yet caps reward multipliers at the first $5,000 per category each month and locks redemption for 12 months.

- Rippling offers the highest confirmed flat rate, up to 1.75% cash back, though its value depends on already running payroll and HR within Rippling.

- Rho bundles banking, cards, and AP automation with no subscription fees and may approve companies that Ramp and others have declined.

6 best Brex alternatives at a glance

Each platform in this list serves a different type of company. Some are built for bootstrapped teams that need a free corporate card with accounting integrations and no funding requirement. Others target funded startups that want banking and cards under one roof.

We narrowed the list by focusing on what truly matters when you're managing spend approvals and reconciling transactions at month-end.

We focused on five criteria:

- Base pricing

- Qualification requirements

- Accounting integrations (which systems and at what plan tier)

- Cash back or rewards structure and complexity

- AP automation depth and support quality based on published user reviews

With these, here’s a quick comparison across the six platforms:

| Platform | Best for | Base price | Cash back | Key note |

|---|---|---|---|---|

| Ramp | Automation-first finance teams | Free; $15/user (Plus) | Automatic cash back | No personal guarantee required |

| BILL Spend & Expense | Bootstrapped, revenue-funded teams | Free | Up to 7x (tiered, complex) | 12-month redemption hold applies |

| Mercury | Startups wanting banking + cards | Free; $35/mo (Plus) | 1.5% flat | The partner bank had a 2024 consent order |

| Rippling | HR-integrated spend management | No per-card fee | Up to 1.75% flat | Best if already on Rippling HR |

| Rho | Flexible qualification needs | Free | Up to 1.5% | Banking + cards + AP in one platform |

| Airbase (Paylocity) | Mid-market AP automation | Custom quote | Not published | Deep AP and procurement workflows |

Ramp, BILL Spend & Expense, Mercury, Rippling, Rho, and Airbase differ most on pricing, qualification rules, accounting integration depth, and AP capabilities. Let’s explore each one in enough detail to narrow the shortlist.

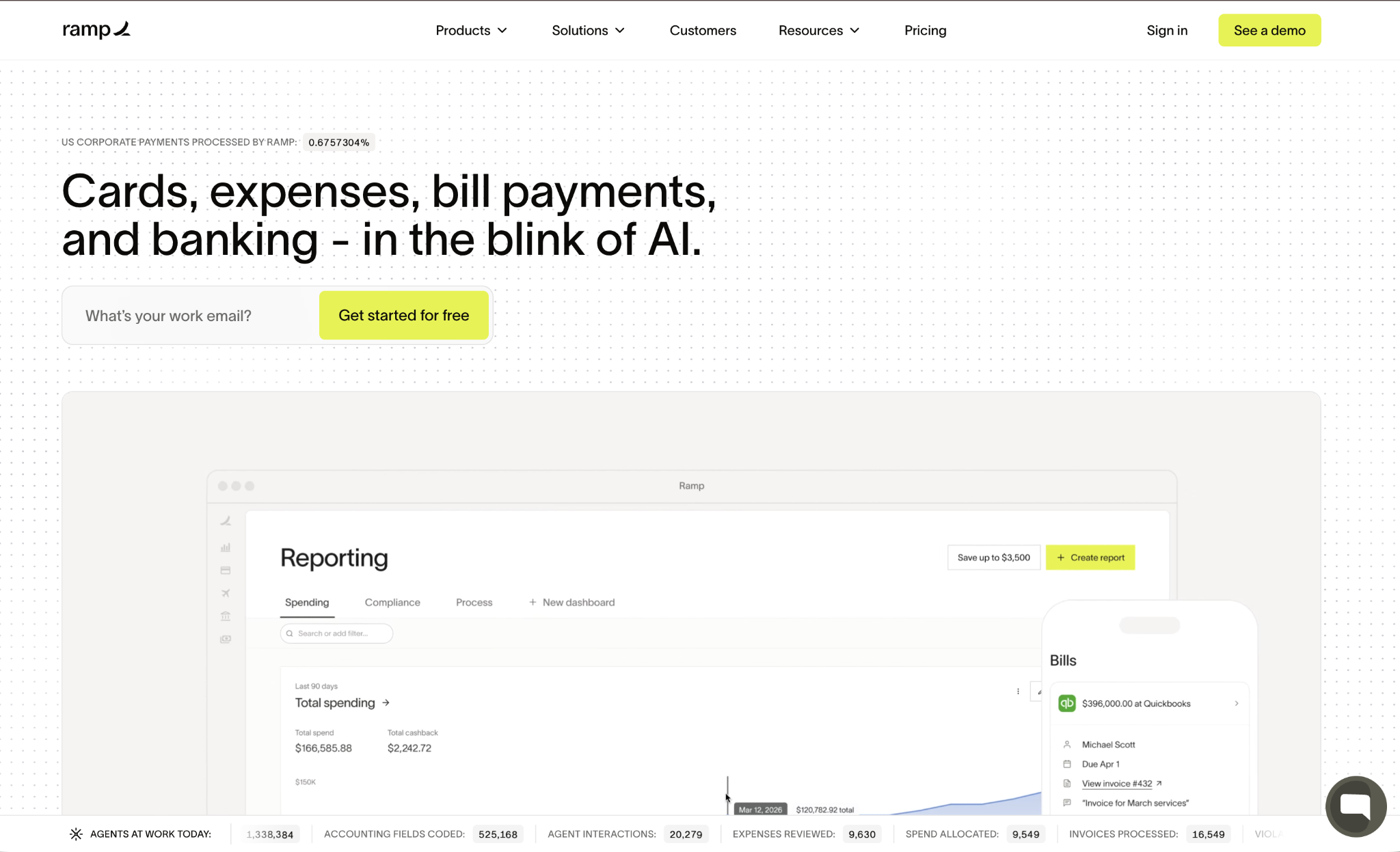

1. Ramp

Ramp is a spend management and AP automation platform with treasury services through First Internet Bank of Indiana, Member FDIC.

The free plan covers unlimited physical and virtual cards, bill pay, auto-receipt matching, QuickBooks Online and Xero sync, and automated expense categorization with no onboarding fees, no contract, and no per-user charges.

Ramp Plus adds NetSuite and Sage Intacct integrations, multi-entity support, and more granular approval workflows at $15 per user per month.

For finance teams in the 50 to 500 employee range, Ramp's free tier covers most day-to-day spend management without requiring a dedicated AP platform. Card-level controls let you set per-card limits, block merchant categories, and auto-lock cards when receipts are missing, all from the same dashboard where AP is processed.

Ramp pros:

- Automatic cash back: Earned automatically on qualifying purchases with no redemption steps or holding periods.

- Free tier depth: Unlimited cards, receipt matching, and basic approval workflows at $0/user/month.

- Card-level controls: Per-card limits, merchant category blocks, and auto-lock when receipts are missing.

- No personal guarantee required.

Ramp cons:

- ERP integrations gated to Plus: NetSuite and Sage Intacct require the $15/user/month plan.

- Sole proprietors excluded: Only U.S.-registered corporations, LLCs, and LPs qualify. A $25,000 minimum bank balance is required.

- Requires a separate bank account: Ramp is a spend layer, not a standalone banking replacement for operating funds.

Pricing: Free for unlimited cards, bill pay, and QuickBooks/Xero sync. Plus runs at $15/user/month, with a discount for annual billing and a 30-day free trial.

Best for: Companies with 50 to 500 employees that want automated receipt matching, real-time spend controls, and AP automation without a personal guarantee or per-user fees.

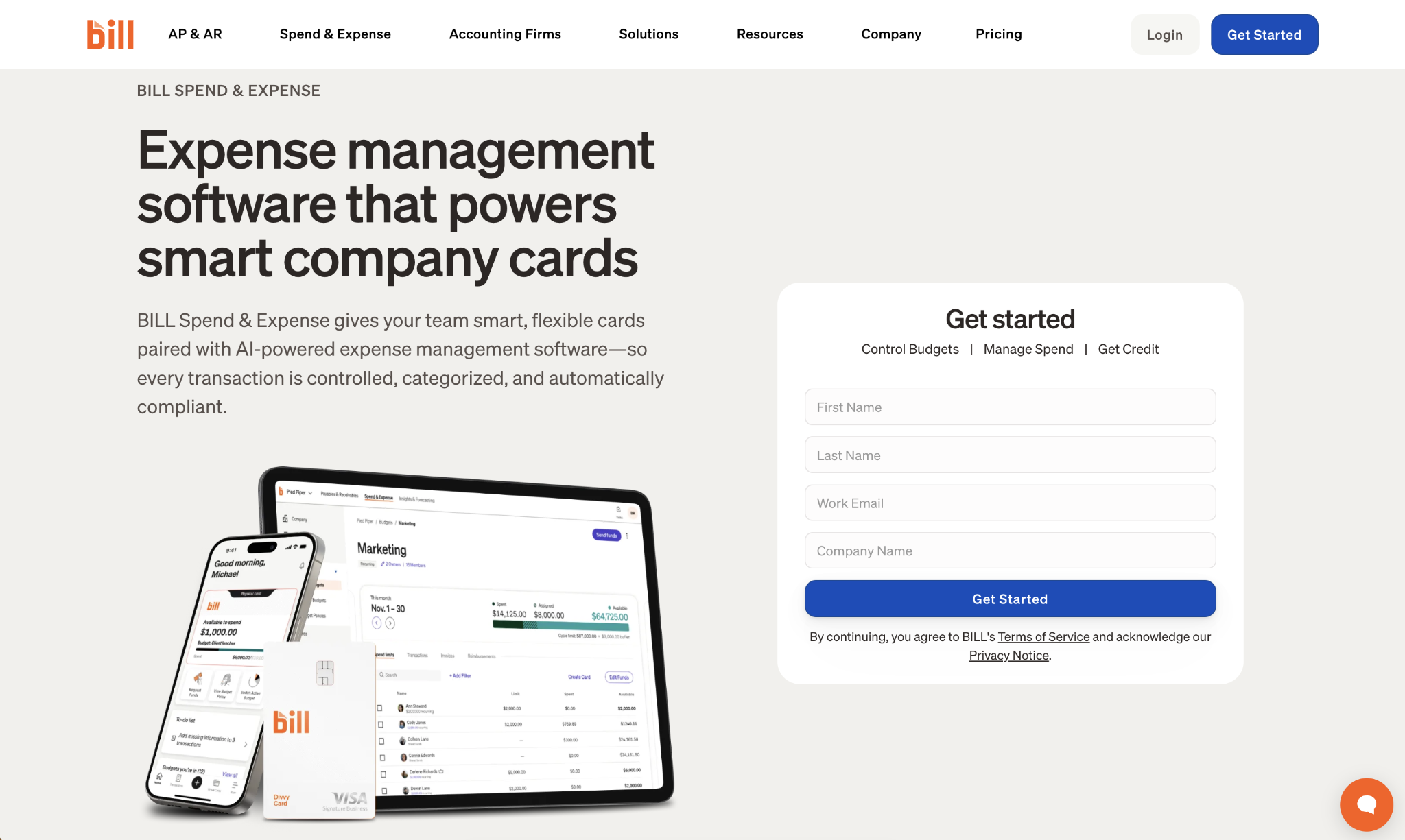

2. BILL Spend & Expense

BILL Spend & Expense (formerly Divvy) is a free corporate card and budgeting platform built around real-time budget enforcement.

When an employee swipes a card, the charge is deducted from the assigned department budget immediately and is auto-declined if it would exceed the limit. BILL Spend & Expense integrates with NetSuite, Sage Intacct, Xero, and QuickBooks at no extra cost.

Approval is based on your business's cash flow and bank balance rather than on outside funding, which sets it apart from Brex's funding requirements. Qualification typically requires a registered U.S. business entity and either roughly $20,000 in a business bank account or steady monthly cash flow, not venture backing.

Rewards are points-based with tiered multipliers by category and payment frequency: up to 7x at restaurants and 5x at hotels, but only on the first $5,000 spent in each category per month. Cardholders must also spend at least 30% of their credit line each month to retain earned points and cannot redeem rewards during the first 12 months after account opening.

BILL Spend & Expense pros:

- Free ERP integrations: NetSuite, Sage Intacct, Xero, and QuickBooks are all included at no cost.

- Real-time budget enforcement: Live Budgets deduct from department limits at the card swipe and auto-decline out-of-policy spend.

- No funding requirement: Approval is based on business cash flow and bank balance, not venture, angel, or accelerator backing.

BILL Spend & Expense cons:

- Complex rewards structure: Multipliers cap at $5,000 per category per month, points are forfeited if spend falls below 30% of the credit line, and redemption is locked for the first 12 months.

- Module-switching friction: Switching between the card and AP/AR modules can disrupt workflows.

- Support response times: Slower than expected for some users, according to published reviews.

Pricing: The core Spend & Expense plan is free. The Corporate plan with full AP/AR runs $89/user/month. The free plan covers expense management and card controls.

Best for: Bootstrapped and revenue-funded companies, and teams on NetSuite or Sage Intacct that need ERP integration without paying per-user fees.

3. Mercury

Mercury is a fintech platform that provides business banking through FDIC-member partner banks, including Choice Financial Group and Column N.A.

The IO Card earns 1.5% cash back on qualifying purchases with no annual fee, and Mercury offers up to $5 million in FDIC coverage through a bank sweep network. The free plan includes checking, savings, and the corporate card with no monthly fee and no minimum balance.

Mercury Plus at $35/month adds advanced invoicing, ACH debit collection, and expense reimbursements for teams with more than 5 active users. Mercury Pro at $350/month includes unlimited invoicing, ACH debit with no transaction fees, NetSuite integration, a dedicated relationship manager, and support for large teams.

One of Mercury's banking partners, Choice Financial Group, received an FDIC consent order in early 2024 tied to its anti-money-laundering controls and oversight of third-party partnerships, which is worth factoring into deposit decisions.

Mercury pros:

- Banking and cards together: Checking, savings, treasury, and a 1.5% cash-back card in one platform.

- Free domestic and USD wires: Both domestic and international USD wires (SHA) are included at no charge.

- High FDIC coverage: Up to $5 million through automatic sweep across partner banks.

Mercury cons:

- Limited expense management: No AP automation, and reimbursements are capped by plan tier.

- Partner bank consent order: Choice Financial Group's 2024 FDIC order over AML and third-party oversight is worth monitoring.

- Cash deposits not supported: Mercury is entirely cashless.

Pricing: Free for banking and card access. Mercury Plus at $35/month. Mercury Pro at $350/month with NetSuite integration and a dedicated relationship manager.

Best for: Funded startups that want banking and a corporate card under one roof and whose primary need is treasury management rather than spend automation. You can also review Mercury alternatives for options with deeper AP capabilities.

4. Rippling

Rippling is an HR platform that added a corporate card to its suite.

When you hire someone in Rippling's HRIS, the system automatically provisions a card, and when someone terminates, the card deactivates on their last day. This lifecycle integration makes card management a byproduct of HR operations rather than a separate admin task.

The card offers up to 1.75% flat cash back, with no per-card fee, no personal guarantee, and no charge for card transactions. Rippling's broader Spend software (expense management and bill pay) is sold as part of its platform, with pricing available only through sales.

For teams already using Rippling for payroll and HR, the benefits of consolidation are clear. For companies not already on the platform, the value case depends on whether the HR integration justifies adopting a new system rather than just a card.

Rippling pros:

- Up to 1.75% flat cash back: Highest confirmed flat rate among the platforms in this comparison.

- HRIS-linked card provisioning: New hires get cards automatically; terminated employees lose access immediately.

- No personal guarantee required.

Rippling cons:

- No banking product: Requires a separate business bank account.

- Opaque platform pricing: Subscription costs aren't published; a sales conversation is required.

- Value is narrower without existing Rippling adoption: Companies not already on the platform must first adopt the full HR suite.

Pricing: No per-card fee. Platform subscription pricing is not publicly available. Contact Rippling directly for a quote.

Best for: Companies already running HR and payroll in Rippling that want automated card provisioning tied to their employee lifecycle.

5. Rho

Rho bundles banking, corporate cards, and AP automation in a single platform with no subscription fees.

There is no annual card fee and no per-transaction charge on standard payments. Rho may be worth evaluating if other platforms have rejected your application due to qualification requirements. Its eligibility criteria appear more flexible than Ramp's for companies without significant bank balances or outside funding.

Third-party review coverage for Rho is thinner than for Ramp or BILL, which makes independent due diligence harder. Eligibility requirements for international founders and companies without a U.S. office are not clearly stated in public sources, so companies in those situations should verify directly.

Rho pros:

- No fees: No subscription, no annual card fee, no per-transaction charges on standard payments.

- Full-stack platform: Banking, cards, AP, and expense management in one place.

- Potentially more flexible qualification: Worth evaluating if other platforms have declined the application.

Rho cons:

- Fewer third-party reviews: Less independently reviewed than Ramp or BILL, making due diligence harder.

- International eligibility unclear: Requirements for founders or companies without a U.S. office are not clearly documented.

- Cash back details are harder to verify: The "up to 1.5%" rate is harder to evaluate from third-party sources.

Pricing: Free. No subscription fee.

Best for: U.S.-based companies that want banking, cards, and AP automation bundled together with no subscription fees, and who may have been declined by other platforms.

6. Airbase (Paylocity)

Airbase (now part of Paylocity following its acquisition) combines expense management, corporate cards, AP automation, guided procurement, and headcount planning into a single platform.

Three-way PO matching, approval workflows mirrored to your org structure, and real-time payables visibility distinguish it from card-first spend platforms. Pricing is quote-based, so finance teams should contact sales for current details.

For mid-market teams with complex approval chains and procurement workflows, Airbase's depth is harder to replicate on a card-first platform. The tradeoff is setup complexity and the time required to configure approval workflows correctly at the start.

Airbase pros:

- Deep AP automation: Three-way PO matching, org-structure-mirrored approval workflows, and real-time payables visibility.

- Guided procurement: Centralized purchase request intake with role-based workflows for finance, legal, IT, and procurement.

- Broad accounting integrations: Compatible with multiple ERP systems; verify current integration details with the vendor.

Airbase cons:

- No public pricing: Requires a sales conversation and a custom quote.

- Setup complexity: Auto-categorization may require manual adjustment; onboarding takes longer for companies with complex approval chains.

- Acquisition uncertainty: Product roadmap priorities may shift over time following the Paylocity acquisition.

Pricing: Custom and quote-based only. Contact Paylocity directly.

Best for: Companies with 150 to 500 employees that need deep AP automation and procurement controls rather than just card spend tracking. If you’re researching alternatives to standalone AP tools, you can explore our SAP Concur alternatives.

How to choose the right Brex alternative

To choose the right Brex alternative, your company's funding stage is the first filter:

- Venture-backed companies qualify for every platform on this list

- Revenue-funded and bootstrapped teams narrow to Ramp, BILL Spend & Expense, and Rho

The second filter is your accounting system:

- On QuickBooks or Xero, Ramp's free tier covers most needs without per-user fees

- On NetSuite or Sage Intacct, or planning to migrate, BILL is the only free option that includes ERP sync

- Ask any vendor whether their integration is two-way, line-item-level, and live rather than scheduled, and whether you can map it to your existing chart of accounts

If your team is growing fast and already using Rippling for HR, the automated card provisioning may justify staying in the ecosystem. If your primary need is corporate card banking alongside spend automation, Mercury is a cleaner fit. If you need AP and procurement controls beyond card management, Airbase warrants evaluation.

For most teams leaving Brex, Ramp is the closest like-for-like replacement, pairing a free corporate card with automated receipt matching and real-time spend controls while asking for no funding history or personal guarantee.

If your books run on QuickBooks or Xero and you want spend management up and running within a few days, you can start with Ramp's free plan and add Plus only when you need NetSuite or Sage Intacct.

Frequently asked questions about Brex alternatives

These questions most often arise for finance managers evaluating their options after leaving Brex or being declined.

Can bootstrapped companies still sign up for Brex?

Generally not. Brex stopped serving most unfunded businesses in June 2022 and now focuses on companies with professional funding from VC, angel, or accelerator investors. However, it also considers businesses that meet other criteria, such as revenue or headcount thresholds. BILL Spend & Expense and Rho are among the more accessible alternatives for bootstrapped and revenue-funded teams.

What happens to Brex accounts after the Capital One acquisition?

Capital One completed its $5.15 billion acquisition of Brex on April 7, 2026, so Brex now operates under Capital One rather than independently. Companies concerned about continuity or roadmap changes can evaluate alternatives proactively and run both platforms in parallel during the transition to minimize disruption.

Do any Brex alternatives require a personal guarantee?

Ramp, BILL Spend & Expense, and Rippling all state that no personal guarantee is required. Airbase uses custom quoting, so specific contract terms should be confirmed directly. Qualification is generally based on business financials rather than your personal credit score.

Which Brex alternative offers the highest cash-back rate?

Rippling currently offers the highest confirmed flat rate at up to 1.75% on all purchases. Mercury's IO Card returns 1.5% flat. BILL Spend & Expense uses a points-based structure with category multipliers up to 7x at restaurants. Still, multipliers apply only to the first $5,000 spent per category per month, and points cannot be redeemed for the first 12 months after account opening.

Which Brex alternative is easiest to set up without a dedicated finance team?

Ramp is a self-serve platform that can be operational within days. The free plan includes automated receipt matching and QuickBooks/Xero sync out of the box, with card-level spend controls that don't require a finance ops background to configure. BILL Spend & Expense is also positioned as accessible, though the rewards structure requires more attention to manage effectively.