AI Systems in Accounting and What Ramp Stack Signals for Finance Teams

June 19, 2026

Most finance teams are already using AI in accounting, but almost none of them are running an AI system. There's a difference, and it's the difference between a ChatGPT tab open next to the general ledger and a platform that executes work against the books with rules and an audit trail.

The question worth asking isn't whether to use AI in your close, since most teams already are, but whether the AI you're using is a collection of point tools or a connected system.

In this guide, we explore what distinguishes an AI accounting system from scattered AI features, what a real one must include, and what Ramp's Stack signals about where the category is headed.

Key takeaways:

- An AI accounting system executes end-to-end work against the books with rules and an audit trail, which is the line that separates it from AI features like categorization, OCR, or a chatbot bolted onto existing software.

- Stitched-together AI breaks down in accounting because the tools aren't connected to the general ledger, aren't auditable, and recreate the manual work they were supposed to remove.

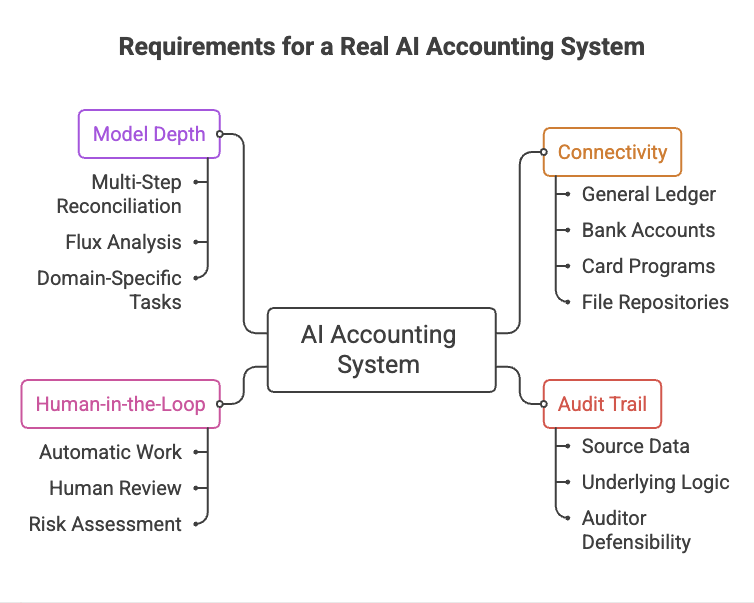

- A real AI accounting system requires connectivity to every system the books touch, a full audit trail on every agent action, human-in-the-loop controls, and accounting-grade model depth rather than a general-purpose model.

- Ramp launched Stack as an AI-native platform for accounting firms, where Stack outperformed every general-purpose model on a Ramp-published benchmark of 200-plus accountant-built tasks.

- Whether you run books in-house or outsource to a firm, the four requirements above are the evaluation checklist, since an outsourced firm's AI infrastructure now affects your close and your audit trail.

What is an AI accounting system?

An AI accounting system is a connected platform where AI agents perform comprehensive accounting tasks on your books, follow rules set by the finance team, and leave an audit trail for every action. That last part is what separates a system from a feature.

AI features like transaction categorization, receipt OCR, or a chatbot that answers questions are useful. But each handles a slice of the task and hands the rest back to a person, whereas a system runs the task from start to finish and shows its work.

The distinction matters because the two get marketed the same way. Almost every accounting tool I’ve seen recently now advertises AI, and most of what they mean is a feature layered onto cash-basis bookkeeping software.

In my experience, the test that cuts through the marketing is simple. Whether the AI can complete a reconciliation or a journal entry end-to-end and produce a record an auditor would accept. Or whether it speeds up one step and leaves a person to stitch the rest together.

Why stitched-together AI breaks down in accounting

The common failure mode I see is a finance team running five or six AI tools that don't talk to each other or to the general ledger. A categorization tool here, a chatbot there, a folder of CSVs exported from one system and imported into another, and the team ends up doing the integration work by hand.

Two problems matter most when AI tools aren't connected:

- The auditability gap: When a tool makes a categorization or posts an entry, "the AI did it" is not an answer an auditor will accept. Tools that can't trace each action back to its source data create exposure rather than removing it.

- The data-silo problem: Disconnected tools force the finance team to manually move data between systems, recreating the reconciliation and re-keying work the tools were bought to eliminate.

Both problems trace back to the same root: the tools were built as features rather than as a connected system. That distinction is what the next section turns into an evaluation checklist.

What a real AI accounting system requires

A real AI accounting system has to clear four bars, and these apply to any tool a finance team evaluates. The teams I've watched evaluate AI accounting tools well treat these as pass-fail requirements rather than nice-to-haves.

Connectivity to every system the books touch

The system has to connect to the general ledger, bank accounts, card programs, and file repositories the books depend on, because an AI agent that can't see every system the books touch can only do part of the work.

A reconciliation tool that connects to the bank feed but not the GL leaves the finance team to bridge the two by hand, which is the manual work that was supposed to disappear. In my experience, this requirement separates a system from a feature faster than any other requirement does.

A full audit trail on every agent action

Every action an agent takes must be traceable to the source data and the underlying logic, since accounting work must be defensible to auditors, lenders, and regulators. A system that posts an entry without a record of why it posted it has created a future problem rather than solving a present one.

The standard I'd hold any AI accounting software to is whether an auditor could follow the agent's work from output back to source without asking a human to reconstruct what happened.

Human-in-the-loop controls

The system must allow the finance team to decide which work runs automatically and which pauses for human review, since not every task carries the same risk. Coding a routine vendor charge is low-stakes and safe to automate, whereas a large or unusual journal entry should be paused for sign-off.

My read after watching teams adopt these tools is that the ones who trust the system fastest are the ones who started with tight human-in-the-loop controls and loosened them as the agent earned trust, rather than turning everything autonomous on day one and getting caught off guard.

Accounting-grade model depth

A general-purpose model can draft an email or summarize a document. Accounting work requires depth across a broader range of domain-specific tasks than a general model can reliably handle.

The difference shows up in tasks that look simple but aren't, like a multi-step reconciliation with exceptions or a flux analysis that has to explain variance rather than just calculate it. The question I'd put to any vendor is how the underlying model performs on accounting tasks rather than on general benchmarks.

Ramp Stack and the shift to agent-based accounting

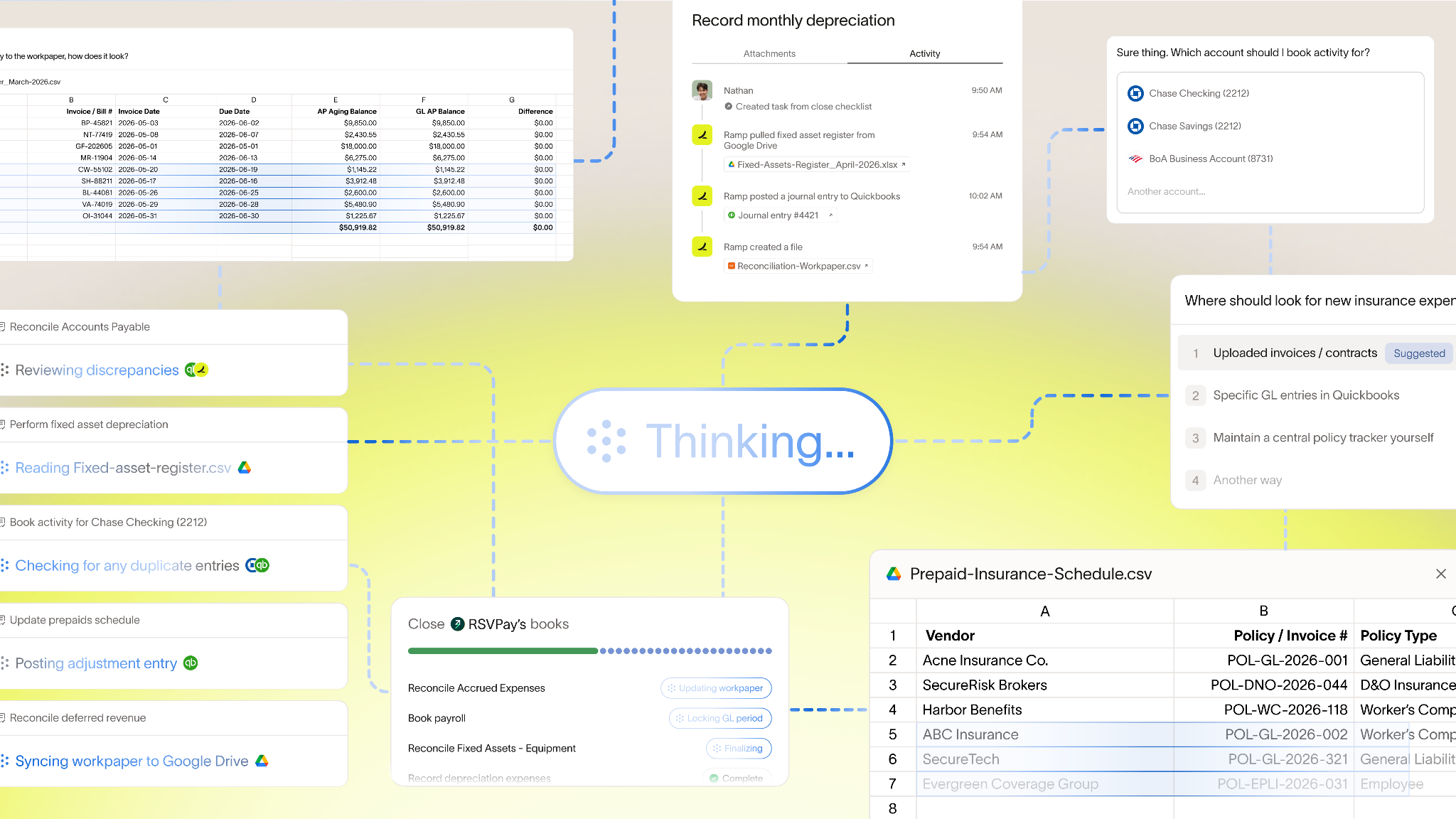

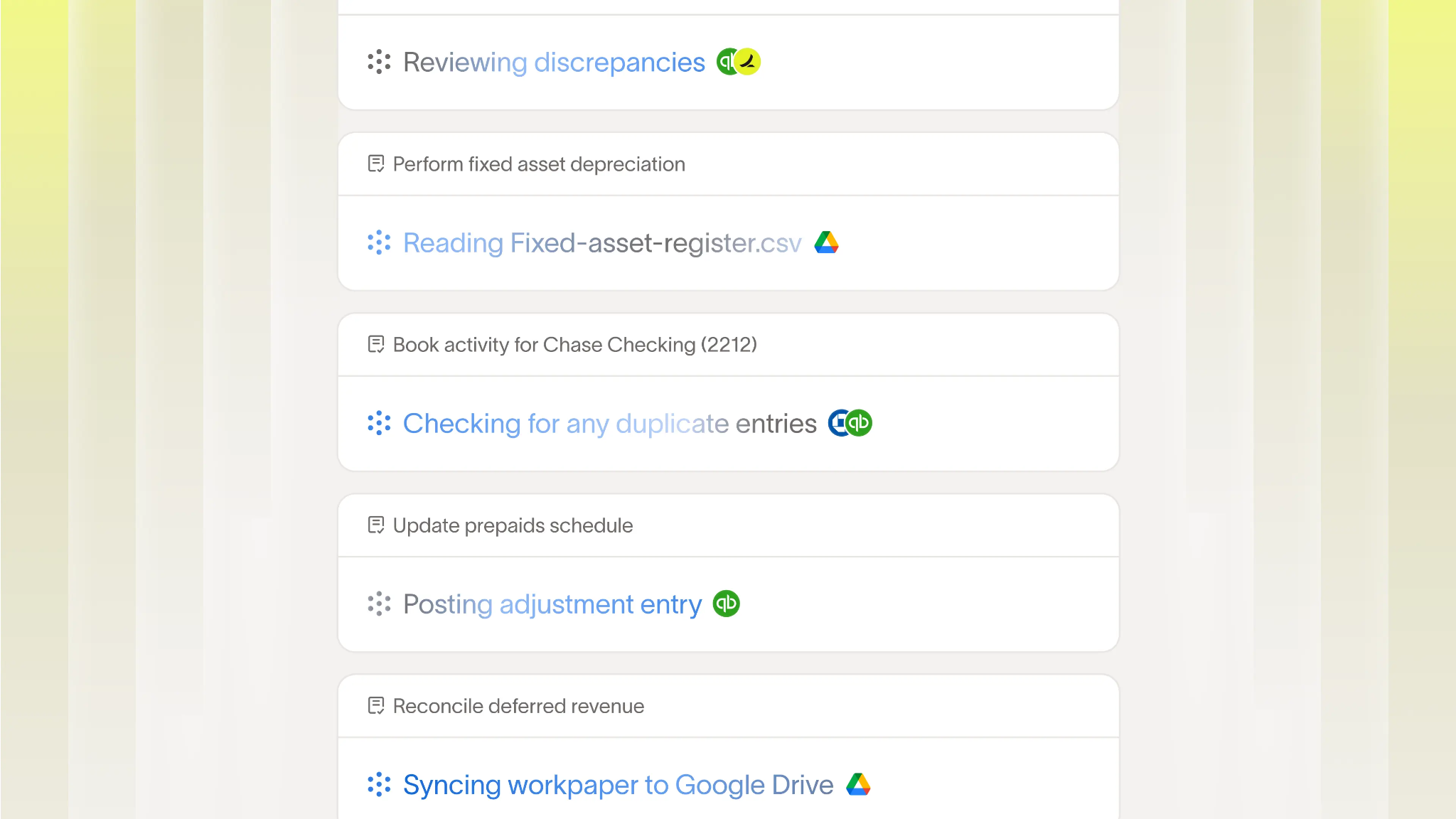

The clearest signal that AI in accounting is moving from features to systems came on June 3, 2026, when Ramp launched Stack, an AI-native platform that lets accounting firms deploy agents to run reconciliations, post journal entries, update schedules, and produce flux and variance analysis, all rule-driven, firm-configured, and auditable.

It's Ramp's first product built for the accounting firm market, and it maps almost cleanly onto the four requirements above, which is why it's worth reading as a category signal rather than a single product release.

On the benchmark, the honest framing matters. Ramp published a benchmark of 200-plus tasks built and graded by working accountants, on which Stack outperformed every general-purpose model evaluated.

That's a meaningful result, but it's a Ramp-published benchmark rather than third-party independent verification. So, the right way to read it is as a strong vendor claim backed by an accountant-built methodology, not as settled external proof.

How the agent model works

The mechanism is what makes Stack a system rather than a feature. Firms teach Stack their processes in plain-English rules, and Stack captures those processes as reusable skills. This functions as standard operating procedures that carry over from one client to the next.

A central Advisor Console is where the team reviews agent work, tags approvers, and decides what runs automatically versus what pauses for sign-off, which is the human-in-the-loop control the category requires. Ramp reports that some firms have seen close times drop by roughly 50%.

My take on what this changes

Here's my honest read after a decade in finance ops. Agent-based accounting is real for a specific slice of work and oversold for the rest. I'd trust an agent to run a routine bank reconciliation, code recurring vendor charges, and draft standard journal entries unattended today. These are repeatable tasks with clear right answers and a clean audit trail.

I would not yet hand an agent the judgment calls, like how to treat an ambiguous accrual, a contract with unusual revenue recognition terms, or anything where the right answer depends on context the model can't see.

The part of the Stack model I find most convincing is the consistency. Working accountants flagged that the real win is the same process running identically across every client, which is the thing that breaks first in a firm scaling faster than it can hire.

The thing I'd watch is the trust curve. The teams that win with this start narrow, keep humans in the loop on anything material, and expand the agent's autonomy only as it earns it. The ones that get burned are the ones that flip everything to autonomous on day one because a benchmark told them it was safe.

What AI in accounting means for your finance team

Whether you run your books in-house or outsource them, the shift to AI systems changes how you should evaluate the tools in your stack. The four requirements above are the same checklist either way, and the operators I work with who handle this well apply it before signing anything rather than after the first close goes sideways.

If you run books in-house

Evaluate any AI accounting tool against the four requirements before you buy, since a tool that misses connectivity or auditability will push work back onto your team in ways that aren't obvious in a demo.

Start the pilot on low-risk, repeatable tasks like bank reconciliation or recurring transaction coding, and keep tight human-in-the-loop review. At the same time, the agent earns trust and only widens its autonomy once you've seen a clean close run through it.

The mistake I'd steer you away from is piloting on your hardest workflow first, because that's the one most likely to need the judgment calls AI isn't ready for.

If you outsource to a firm

Your firm's AI infrastructure now affects your close and your audit trail, which makes their stack your concern even though you don't run it.

The questions worth asking are:

- Whether their AI is connected to your general ledger or stitched together from point tools

- Whether every agent action produces an audit trail you could hand to a lender, and where they keep a human in the loop.

A firm running on a real system should be able to answer all three without hesitation, and in my experience, the quality of that answer tells you more about the firm than any pitch deck.

Pick the system, not the feature

AI in accounting is shifting from scattered features to connected operating systems, and the teams and firms that build on real infrastructure are the ones that compound the gains rather than recreating manual work at higher speed.

The four requirements, which are connectivity, auditability, human-in-the-loop control, and accounting-grade model depth, are the evaluation criteria whether you're assessing a tool for your own close or asking your outsourced firm about theirs.

If you want to see what a platform built at this frontier looks like in practice, you can try Ramp Stack for free, a low-risk way to test the four requirements against a real close before you commit.

Frequently asked questions about AI systems in accounting

Can AI agents replace accountants?

AI agents can run repeatable, rule-based work like reconciliations and routine journal entries, but they can't yet handle the judgment calls accounting depends on. The realistic near-term model keeps accountants in the loop on anything material while agents absorb the high-volume, low-ambiguity work that consumes most of the close.

Is AI-generated accounting work auditable?

AI-generated accounting work is auditable only when the system traces every action back to source data and the logic behind it. A tool that posts an entry without a defensible record creates audit exposure rather than removing it, which is why a full audit trail is a pass-fail requirement when evaluating any AI accounting platform.

What is the difference between using ChatGPT and an AI accounting platform?

ChatGPT is a general-purpose model that can answer questions and draft text but isn't connected to your books and leaves no audit trail. An AI accounting platform connects to your general ledger and systems, executes complete tasks, and records every action, which is the difference between a feature that speeds up one step and a system that runs the work.