What Should You Use Instead of Mercury When Your Finance Stack Starts to Matter?

May 18, 2026

Mercury works well for early-stage companies building their first banking setup, but growing teams often hit its limits faster than expected. At $350/month for Mercury Pro for their most advanced NetSuite automations, a dedicated relationship manager, and higher reimbursement limits, and a five-user cap on free expense reimbursements, the platform ends up pricing out the segment it was designed for.

In this article, we compare 5 Mercury alternatives on pricing, FDIC coverage, integrations, and where each fits in your finance stack: Ramp, Rho, Relay, Bluevine, and Arc. You’ll learn how to choose with a decision framework by company stage and priority.

In brief:

- Ramp covers expense management, AP automation, and corporate cards in a free platform with accounting sync for QuickBooks, Xero, NetSuite, and Sage. A Ramp Treasury account, launched in January 2025, extends the platform into banking for companies seeking further consolidation.

- Rho offers banking, corporate cards, AP automation, and expense management with $0 platform fees, including NetSuite and Sage Intacct at no extra cost. The $75M in FDIC sweep coverage is the highest on this list by a wide margin.

- Relay lets you open up to 20 checking accounts under one company for true cash segmentation with automated transfer rules. It's the right fit for Profit First practitioners and teams that want real, separated balances rather than virtual budget buckets.

- Bluevine is the only platform here that pairs high-yield checking (3.0% APY on Premier) with a built-in business line of credit up to $250K. For teams maintaining $100K or more in their operating account, the fee waiver makes the economics work.

- Arc suits VC-backed SaaS companies with meaningful cash balances that need treasury yield, revenue-based financing, and an AI monitoring layer in one platform. The Standard plan is free; the invite-only Platinum tier starts at $249/month with up to $5.25M in FDIC coverage.

A quick overview of the best Mercury alternatives

In this list, Ramp and Rho sit at the full-stack end, covering expense management, AP and banking. Relay excels at cash segmentation, Bluevine pairs high yield with built-in credit access, and Arc is built narrowly for venture-backed tech companies with idle capital to deploy.

Here’s a quick side-by-side to help you narrow the list:

| Platform | Best for | Base price | Full banking replacement? | FDIC coverage |

|---|---|---|---|---|

| Ramp | Expense automation, AP, spend visibility | Free core | Partial (Treasury added Jan 2025) | Verify directly |

| Rho | Integrated stack with no platform fees | Free core platform | Yes | $75M |

| Relay | Multi-account cash organization | Free (Starter) | Yes | $3M |

| Bluevine | High-yield checking plus credit access | Free (Standard) | Yes | Verify directly |

| Arc | VC-backed SaaS treasury and capital | Free (Standard) | Yes | $5.25M |

Each platform has tradeoffs worth understanding before you commit, so let’s walk through them one by one.

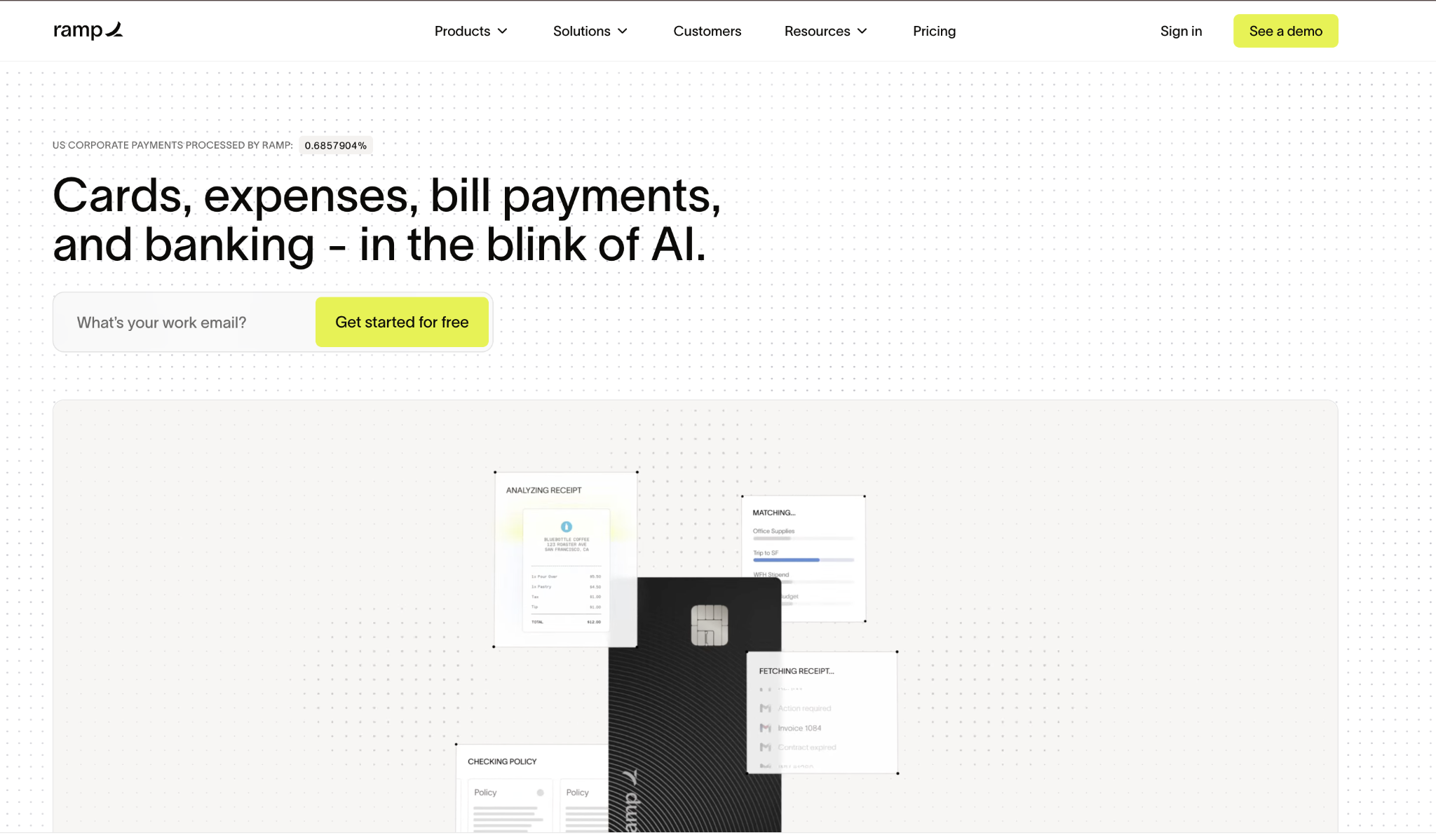

1. Ramp

Ramp is a free spend management platform covering corporate cards, expense management, accounts payable automation, and vendor payments.

The company reached a $32B valuation in November 2025 after doubling revenue and customers year-over-year, now serving more than 50,000 companies with over $100B in annualized purchase volume. The free tier includes all core expense features, and flat cash back applies to all card spend without category restrictions or annual fees.

Ramp expanded into banking with Ramp Treasury in January 2025, adding a business deposit account in partnership with First Internet Bank of Indiana and a money market investment account for higher yields.

The banking layer is newer than the expense tools, so companies looking to replace Mercury entirely should confirm the Treasury account meets their day-to-day checking needs before closing their Mercury account.

Ramp Plus at $15/user/month adds advanced policy controls, procurement workflows, and deeper reporting for finance teams that need more granular spend management. Unlike Mercury, where NetSuite access requires upgrading to the $350/month Pro plan, Ramp includes NetSuite and Sage Intacct integrations at no additional charge.

For teams where the core friction is AP workflows and approval routing rather than banking features, Ramp often resolves the problem without requiring a full banking migration.

Ramp pros:

- Free core platform: Corporate cards, AP automation, receipt capture, and accounting sync with QuickBooks, Xero, NetSuite, and Sage are all included at no subscription cost. There's no per-user cap on core expense features, which matters once your team grows past Mercury's five-user free reimbursement limit.

- No foreign transaction fees: Ramp charges no foreign transaction fees on card spend and earns flat cash back on all purchases, with no category restrictions. That combination outperforms most traditional corporate card programs without any annual fee.

- NetSuite included at no charge: Unlike Mercury, where enriched NetSuite automations start at $35/month on Plus and reach $350/month for Pro with a dedicated relationship manager, Ramp includes NetSuite and Sage Intacct integrations at no additional charge.

- Ramp Treasury: The January 2025 launch added a business deposit account, money market fund, and managed investment account to the platform. Teams already using Ramp for expense management can reduce their reliance on a separate banking relationship for many use cases.

Ramp cons:

- Banking layer is newer: Ramp Treasury launched in January 2025 and is less mature than Mercury's core banking product. Companies with complex banking needs or high transaction volumes should thoroughly test the Treasury account before designating it as their primary checking account.

- Not a full bank replacement for all teams: Depending on your operations, you may still need a separate primary checking account alongside Ramp. It works better as a spend management and AP layer than as a standalone bank for most companies at this stage.

Pricing: The core platform is free with no per-user fees for expense management, AP automation, or accounting integrations. Ramp Plus is $15/user/month for advanced policy controls, procurement workflows, and expanded reporting. Enterprise pricing is custom and includes dedicated support and implementation resources.

Best for: Companies at any stage where finance operations have outgrown spreadsheets and where AP automation and spend visibility are the primary drivers behind evaluating a Mercury alternative.

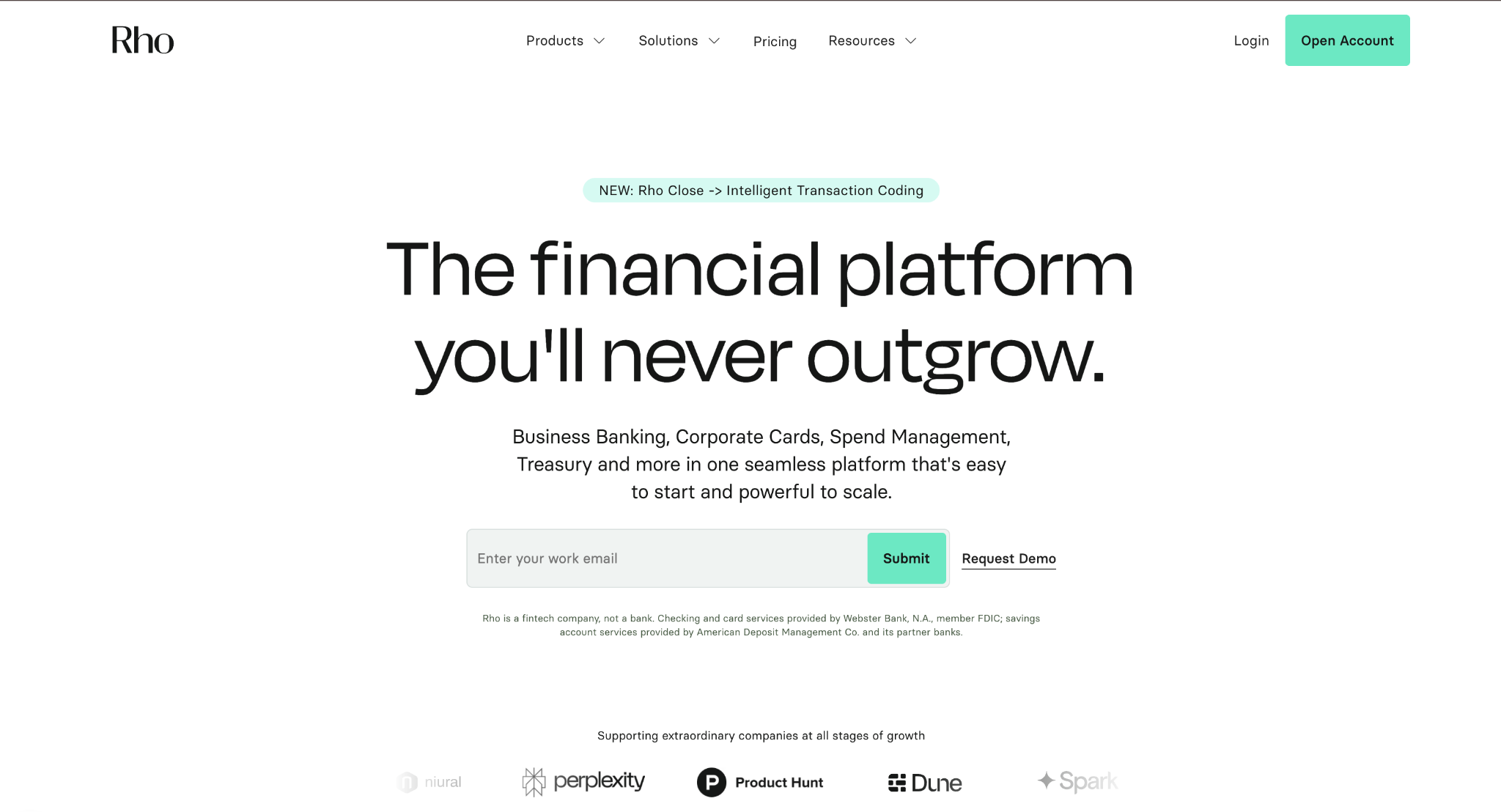

2. Rho

Rho combines banking, corporate cards, expense reimbursement management, AP automation, and treasury into a single platform with $0 platform fees.

Banking services run through Webster Bank, N.A., with FDIC insurance up to $75M available through a sweep network of more than 400 insured banks. NetSuite, Sage Intacct, and AP automation are included at no additional charge, directly addressing Mercury Pro's $350/month ERP cost.

The Rho corporate card earns up to 1.5% cash back on all spend, with scalable credit limits based on full underwriting rather than solely on your cash balance.

All users get 24/7 support at no extra cost, regardless of plan tier, a direct contrast to Mercury's support model, where free-tier customers don't get phone access. Banking, cards, expenses, AP, and treasury all live under a single login, without a separate expense platform to connect to or reconcile.

Rho's treasury product lets you hold idle cash in US Treasury Bills for additional yield while keeping your operating account available for day-to-day payments. The platform is US-focused and has limited international payment capabilities, which matters if your vendors or employees are outside the US.

For companies that regularly pay international contractors or suppliers, pairing Rho with a dedicated FX tool closes that gap without sacrificing the zero-fee domestic stack.

Rho pros:

- $0 for everything: NetSuite, Sage Intacct, AP automation, unlimited expense reimbursements, same-day ACH, and domestic wires are all included with no platform fee. For companies currently paying for these as separate tools or upgrading to Mercury Pro, the cost savings are immediate.

- $75M FDIC coverage: The $75M coverage available through Rho's sweep network of 400+ banks is the highest on this list by a wide margin. For companies holding significant operating cash, that coverage removes a real concern about single-bank concentration risk.

- 24/7 support for all users: Rho provides 24/7 customer support regardless of plan tier, with no feature gating behind a paid upgrade. That's a meaningful advantage over Mercury, where responsive support is tied to the Pro plan.

- Integrated treasury: The treasury product lets you put idle cash to work in T-Bills and money market funds within the same platform. There's no separate brokerage account or treasury management tool to maintain alongside your banking.

Rho cons:

- No ATM access or cash deposits: Rho doesn't support cash deposits or ATM withdrawals, which rules it out for businesses that handle physical cash. If your operations involve retail payments or regular cash handling, you'll need a different primary bank.

- US-focused with limited international reach: Rho's international payment capabilities are limited. Teams with employees or vendors outside the US will likely need a supplemental tool for cross-border payments.

Pricing: $0 platform fee for all users and features across all tiers. Foreign currency transfers carry a 1% fee, and the optional SWIFT payment carries a $15 fee. No monthly charge, no per-user fee, and no upgrade required to access NetSuite integrations or AP automation.

Best for: Growing companies with 50 to 500 employees that need a full financial stack, including ERP integrations and AP automation, without paying per-user or per-feature subscription fees.

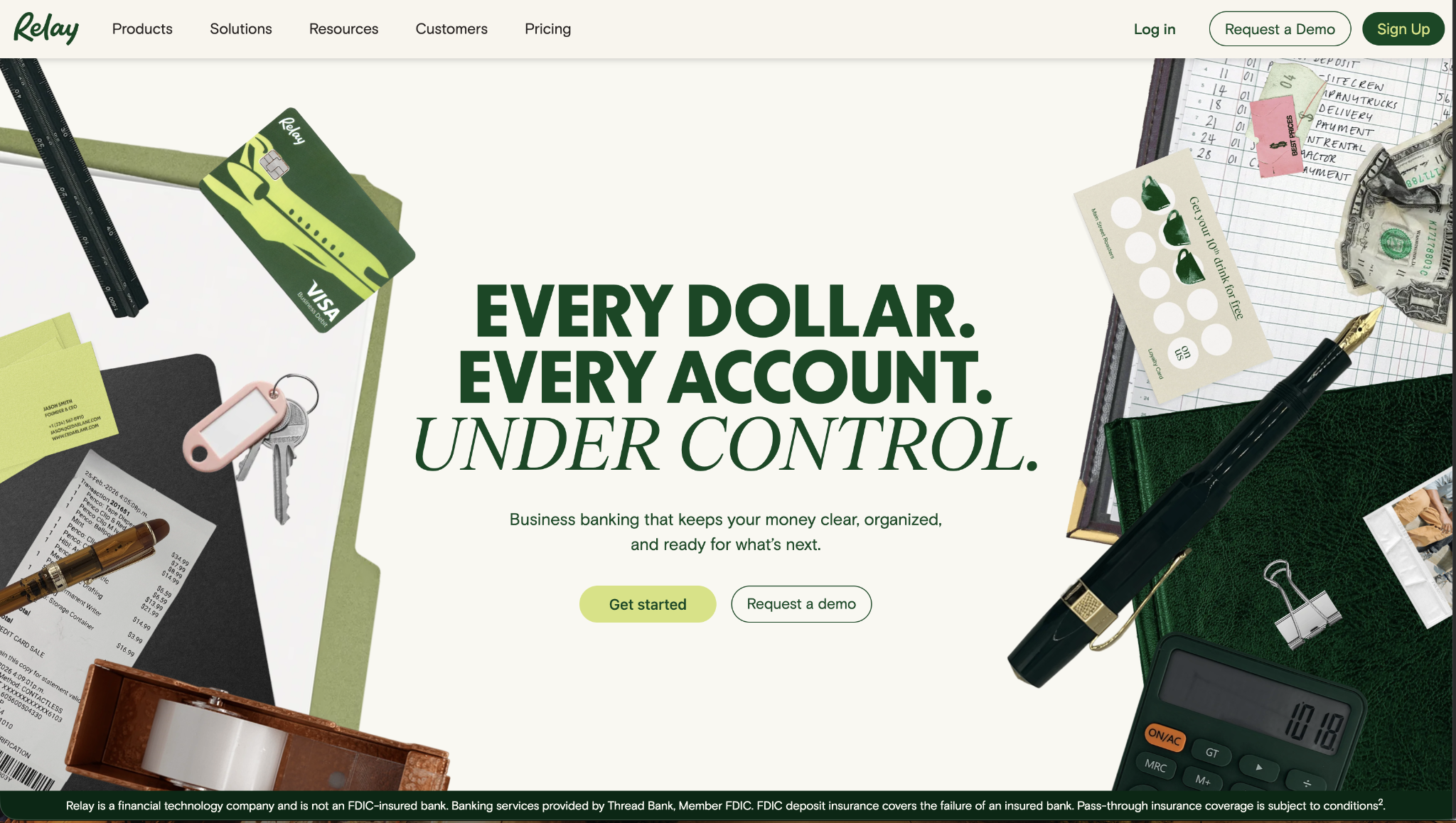

3. Relay

Relay lets you create up to 20 checking accounts under one company, a structure that fits Profit First budgeting or any team that wants to separate operating cash, tax reserves, and payroll into distinct buckets with real, separated balances.

Each account has its own balance and card assignments, so budget categories are actual funds rather than virtual tracking lines within a single account. Automated transfer rules can move a specified percentage of each deposit into designated accounts on your schedule.

Relay supports cash deposits at 90,000+ retail locations across the US, a direct advantage over Mercury, Rho, and Brex, none of which offer in-person deposit access. QuickBooks sync is bidirectional: unpaid bills import from QuickBooks Online into Relay, payments execute through the banking platform, and payment status syncs back automatically.

FDIC coverage reaches up to $3M through Thread Bank's insured cash sweep program, and the FDIC terminated Thread Bank's 2024 FDIC consent order in December 2025, resolving the regulatory issue that some businesses had been monitoring.

The Grow and Scale tiers add phone support and higher account limits, but most core features are available on the free Starter plan. Relay doesn't include lending products, so if you need a credit line alongside your banking, you'll need to maintain that separately.

For companies practicing Profit First or running any cash allocation methodology, Relay's multi-account structure provides a level of cash segmentation that no other platform on this list can match.

Relay pros:

- Up to 20 checking accounts: True cash segmentation with real, separate balances enforces budget categories at the account level rather than just tracking them in a spreadsheet. Automated transfer rules move percentages of incoming deposits into designated accounts as each deposit lands.

- Cash deposit access: Cash deposits are available at 90,000+ retail locations across the US, which puts Relay ahead of Mercury, Rho, and Brex for businesses that handle physical cash. For cash-heavy operations, that access alone narrows the field to Relay and Bluevine.

- Bidirectional QuickBooks sync: Unpaid bills are imported from QuickBooks Online into Relay, payments are executed through the banking platform, and status is automatically synced back. That bidirectional connection is more integrated than most banking-to-accounting connections on this list.

- Thread Bank consent order resolved: Thread Bank received an FDIC consent order in 2024, but the FDIC terminated that order in December 2025. Current regulatory status can be verified at fdic.gov before you open an account.

Relay cons:

- No lending products: Relay doesn't offer a business line of credit or any other lending products. If credit access alongside your banking matters, you'll need to source that separately, and Relay can't consolidate it.

- Phone support requires a Scale plan: Starter and Grow customers get standard support only, with no phone access. For teams managing complex multi-account setups, the $90/month Scale plan may be worth it for the support tier alone.

Pricing: Starter is free with no monthly fee. Grow is $30/month. Scale is $90/month (discounted from $120). Interest is earned only on savings accounts, not on checking balances, so your operating cash earns nothing unless you actively move it to a savings account.

Best for: Companies practicing Profit First or any team that needs granular cash organization across multiple accounts, especially if your operations require cash deposit access that Mercury doesn't offer. For context on what to look for when evaluating a banking partner, our guide on choosing a business bank covers the key due diligence factors.

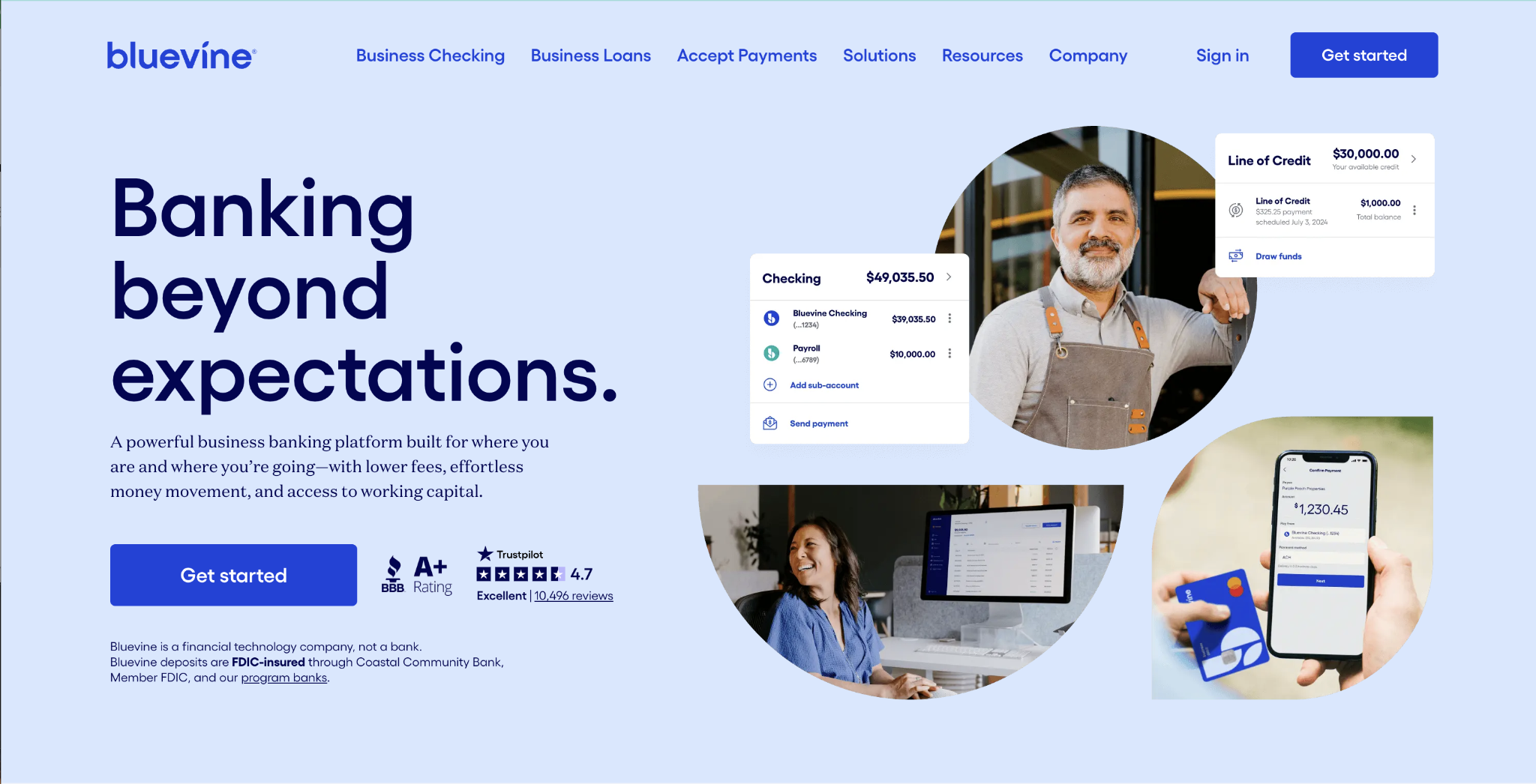

4. Bluevine

Bluevine is the only platform in this comparison that combines high-yield checking with a built-in business line of credit.

The Premier plan earns 3.0% APY directly on your checking balance with no cap, and the $95/month fee is waivable if you maintain a $100K average daily balance and put $5K/month on the Bluevine debit or cash back card.

For companies already holding significant operating cash, that fee structure can effectively make Premier free while earning more on that balance than most business accounts.

Bluevine's business line of credit runs from $5,000 to $250,000 with repayment terms of 6 or 12 months, starting at 7.8% annualized simple interest for top-qualifying applicants. Minimum requirements are a 625 credit score, $120,000 in annual revenue, and 12 months in business.

The Standard plan is free and earns 1.3% APY on your checking balance, which is competitive with most business checking accounts that pay nothing. Bluevine's primary card is a debit card, and the Bluevine Business Cashback Mastercard (a credit card that earns 1.5% cash back) is available by invitation only to eligible checking customers.

Teams that need corporate cards with granular approval workflows or spend controls outside the Bluevine ecosystem may still need a dedicated expense management platform alongside their account.

Bluevine pros:

- 3.0% APY on Premier checking: The Premier plan earns interest directly on your checking balance with no balance cap. For a company holding $200K in operating cash, that's roughly $6,000/year earned on funds that would otherwise sit idle.

- Built-in credit access: A business line of credit up to $250K is available within the same platform as your banking, with rates starting at 7.8% annualized for top qualifying applicants. That integration eliminates the need to maintain a separate lending relationship for working capital.

- Premier fee waiver: The $95/month Premier fee is waivable with an average daily balance of $100K and $5K in monthly debit card spend. Teams that already meet those thresholds pay nothing for the highest-yield plan on this list.

- Standard plan earns yield: The free Standard tier earns 1.3% APY on your checking balance at no monthly cost. That's a useful entry point for companies that don't yet hold enough cash to justify Premier.

Bluevine cons:

- Revenue requirements for waiving the Premier fee: The $100,000 average daily balance threshold excludes many early-stage companies.

- Paid tiers add meaningful monthly cost: Premier's $95/month fee is waivable but requires $100K in deposits and $5K/month in card spend.

- Credit card is invite-only: The Bluevine Business Cashback Mastercard (a 1.5% cash-back credit card) is available by invitation only to eligible checking customers, not on demand. Teams that need corporate cards with granular approval workflows or spend controls outside the Bluevine ecosystem will likely still need a dedicated expense management platform alongside their account.

- Wire and cash deposit fees: Outgoing domestic wires cost $15, and cash deposits cost $4.95 per deposit. For teams making frequent wire transfers or handling regular cash deposits, those fees can add up over the course of a month.

Pricing: Standard is free with no monthly fee and earns 1.3% APY on checking balances. Plus is $30/month. Premier is $95/month, waivable with a $100K average daily balance and $5K per month in card spend, and earns 3.0% APY on all balances with no cap.

Best for: Companies that keep $100K or more in their operating account and want that cash earning yield while also having access to a built-in line of credit, all within the same platform. For a broader view of how Bluevine stacks up against traditional banking, our comparison of business accounts vs fintech solutions covers the key tradeoffs.

5. Arc

Arc is a banking and treasury platform for private companies that need to put idle cash to work. The free Standard tier includes a checking account, treasury access across money market funds and US Treasury Bills, corporate cards, and AR/AP management.

FDIC coverage reaches up to $5.25M through Arc's sweep network, higher than the $2.5M figure that appeared in earlier coverage of the platform. The Archie AI CFO agent, launched in September 2025, provides automated cash flow monitoring, forecasting, and reporting within the platform.

The treasury product offers yield on idle cash through money market funds, Treasury Bills, and mutual funds with customizable auto-transfer rules. That top yield rate requires the $249/month Platinum tier, which is invite-only, and Platinum deposits are held at G-SIBs (Global Systemically Important Banks), an unusual deposit structure compared to standard sweep arrangements.

For companies with meaningful idle cash on the balance sheet, Arc's combination of treasury yield and AI-assisted monitoring is hard to find in a single platform. The platform works best for well-capitalized tech companies where treasury management is a real priority.

Arc pros:

- Archie AI CFO agent: The Archie AI agent, launched in September 2025, provides automated cash flow monitoring, forecasting, and financial reporting within the platform. For companies without a dedicated CFO, that layer of automated oversight covers visibility gaps that would otherwise go unnoticed.

- Revenue-based financing: Non-dilutive capital options are available through Arc Capital Markets, with indicative debt terms for up to $250M from Arc's lender network. For VC-backed companies that want to extend their runway without additional equity dilution, this is a meaningful addition to the platform.

- $5.25M FDIC coverage: Arc's sweep network provides up to $5.25M in FDIC coverage, 21x the standard $250K limit. For startups holding significant capital between funding rounds, that coverage provides real protection against single-bank concentration.

- Automated treasury yield: The platform automates the allocation of idle cash to money market funds and T-Bills using configurable rules. You set the allocation parameters, and Arc handles the execution without manual account management.

Arc cons:

- Accounting integrations unconfirmed: QuickBooks, Xero, and NetSuite integration support couldn't be independently verified through public sources. Confirm these directly with Arc before treating it as your primary accounting workflow platform.

- Top yield rate requires Platinum: The highest treasury yield rates are only available on the $249/month Platinum tier, which is invite-only. Standard tier users earn lower rates until they qualify for an invitation.

Pricing: Arc Standard is free with no monthly fee and includes checking, treasury access, corporate cards, and AR/AP management. Arc Platinum starts at $249/month and is invite-only, offering higher FDIC coverage and top treasury yields.

Best for: VC-backed SaaS and tech startups with meaningful cash balances that need treasury yield, revenue-based financing, and AI-assisted cash flow monitoring in one platform. Our overview of SaaS spend management covers related tools that often complement Arc for teams needing more on the spend side.

How to choose the right Mercury alternative

Banking migrations take work because every automated payment, payroll connection, and vendor ACH relationship has to be updated. Evaluate beyond your current needs before switching, since the right platform should fit where you're going, not just where you are now.

If expense management and AP are your biggest friction points, Ramp solves them at $0 without requiring a full banking migration. If you want a single login for banking, cards, expenses, AP, and ERP integrations with no per-user fees, Rho covers the full stack.

Relay fits cash-heavy operations or Profit First practitioners, Bluevine fits companies holding significant operating cash that want yield plus credit access, and Arc fits VC-backed tech companies with idle capital to deploy.

If the underlying problem is expense workflow friction, invoice approvals, or ERP integration costs, Ramp solves it at no cost and includes NetSuite sync without any paid Mercury plan upgrade.

Frequently asked questions about Mercury alternatives

Is Rho really free for all features?

Rho doesn't charge platform fees for core banking, cards, AP automation, or expense management features. Revenue comes from interchange on card transactions and treasury management fees. Premium features, such as advanced treasury products, may incur additional costs, so confirm the specific features you need before assuming it's entirely fee-free in every use case.

Can I switch banks without disrupting payroll?

You can, but timing matters significantly. Payroll providers like Gusto and Rippling typically require a 2- to 3-day micro-deposit validation period before a new bank account becomes active. Start the switch well before a scheduled payroll run, and keep your Mercury account active until at least two full payroll cycles have successfully processed on the new platform.

Does FDIC insurance protect me if my fintech platform shuts down?

FDIC insurance protects against the failure of the partner bank holding your deposits, not the fintech platform itself. The Synapse collapse in 2024 made that gap clear, with customers losing access to their funds for months even though the underlying banks remained solvent. Confirming that your fintech's banking partner is directly FDIC-insured and that recordkeeping is current is a baseline due diligence step before any migration.

Why do companies leave Mercury?

Commonly cited reasons include the five-user cap on free expense reimbursements, the $350/month cost for Mercury Pro's NetSuite integration, and account restrictions that some businesses should review carefully during due diligence. Growing teams often find that Mercury's banking core is solid, but gaps in AP automation and ERP integration require expensive add-ons, eliminating the cost advantage.

Which Mercury alternative has the highest FDIC coverage?

Rho offers up to $75M in FDIC coverage through its sweep network of over 400 FDIC-insured banks. Brex follows at $6M, then Arc at $5.25M, Relay at $3M, and Mercury itself at $5M standard coverage. Bluevine's coverage through its sweep network is best confirmed directly on Bluevine's site before you commit.